Understanding MVA

BY MARSHALL TILLEY

MVA 101: What is a Market Value Adjustment?

A Market Value Adjustment (MVA) is a feature commonly used in annuity contracts that adjusts the surrender value to reflect changes in interest rates. The first MVAs emerged in the early 1980s in response to a volatile interest rate environment, when the Federal Reserve aggressively raised rates to combat inflation. This era of rapid rate hikes sharply impacted bond values, annuity pricing, and overall market stability. Recognizing the need for a mechanism that could dynamically adjust to these market conditions, insurers introduced MVAs as a risk management tool to protect both the insurer and the broader pool of contract holders.

MVAs are a prevalent feature on modern annuity products, yet they often confuse both advisors and consumers due to their impact on surrender values. Many struggle to distinguish MVAs from traditional surrender charges, leading to misconceptions about their role in annuity pricing. Others are simply confused because MVAs seem complex and are challenging to explain. This unfavorable perception is further reinforced by the fact that insurers typically offer higher rates on products featuring an MVA.

Rather than serving merely as a fee, MVAs adjust an annuity’s surrender value to match the current market value of the underlying investments. This adjustment helps preserve the insurer’s financial balance, which in turn protects the interests of contract holders. In addition, regulatory rules ensure that these adjustments work in both directions, maintaining fairness for both the insurer and the contract holder.

The impact of an MVA depends on the direction of interest rates at the time of withdrawal. Let’s take a closer look at how MVAs function in both rising and falling rate environments.

Rates Up, Adjust Down

MVAs work by linking surrender values to the insurer’s underlying portfolio of assets, the value of which fluctuates with interest rates. When interest rates rise, newly issued assets offer higher yields, making existing lower rate assets less valuable. If contract holders make withdrawals, the insurer will likely need to liquidate the assets backing the contract at a loss—in this case, the insurer would apply a negative MVA to the withdrawal in order to mitigate their loss. This protection is important to insurers because rising interest rate environments tend to lead to more withdrawals, as contract holders search for higher rates. The propensity of surrenders in this scenario is why many view MVA as a fee. However, the negative MVA in rising rate markets works to the advantage of all contract holders who do not surrender, as they are not negatively impacted by the investment loss.

Rates Down, Adjust Up

When interest rates decline, existing higher-yield bonds become more valuable. If the insurer sells assets to fund a withdrawal at this time, they will experience an investment gain—this gain would be passed along to the contract holder in the form of a positive MVA. This creates a dilemma for consumers who hope to optimize their returns with an MVA and transfer into a similar investment. As rates decline and MVA benefits rise, the original contract is increasingly more likely to credit a higher rate than comparable products being offered at that time. The positive MVA is a benefit to client who needs to liquidate their investment for an immediate financial need following a reduction in interest rates—in this scenario the insurer would pass along the MVA as a proxy for the investment gain and the client receives more cash value.

MVA 201: MVA Formula Components

The standard formula for the Market Value Adjustment (MVA) is:

$$\left( \frac{1+I}{1+J} \right)^N – 1$$

Where:

N: The number of years remaining in the MVA period.

I: The reference rate at the start of the MVA period (the rate the asset was earning when the contract was issued).

J: The reference rate at the time of surrender (the current market rate for a bond with the same remaining duration).

The formula works in two steps:

- Accumulation at I:

The asset backing the annuity is assumed to grow at the initial rate I for N years. This step calculates the maturity value the asset would reach if it continued to earn its original rate throughout the period. - Discounting at J:

The maturity value obtained by accumulating at I is then discounted back over N years using the current rate J. This reflects the fact that a bond with the same remaining duration is now earning the rate J.

The difference between I and J drives the MVA adjustment:

If J>I:

The higher current rate leads to a larger discount, reducing the present value of the asset. This produces a negative MVA and lowers the annuity’s surrender value.

If J<I:

The lower current rate results in a smaller discount, increasing the present value of the asset. This produces a positive MVA and raises the annuity’s surrender value

The impact or magnitude of the MVA depends on both the rate differential (I vs. J) and the time remaining (N). Like most investments, the compounding impact of the time value of money leads to a more significant adjustment. If the duration of the hypothetical asset is shorter the impact will be weaker. Typically, the MVA period aligns with the surrender charge schedule.

This process ensures that the value of the asset is first calculated based on its original earning rate and then adjusted to reflect current market conditions.

MVA 301: How MVA Impacts Product Design

MVAs play a critical role in annuity product design. By adjusting surrender values to reflect interest rate movements, MVAs help insurers manage risk while offering contract holders a fair-value exchange for early withdrawals. A properly structured MVA can significantly improve an insurer’s financial position, from how reserves are calculated, to how much capital is required under regulatory frameworks, to how their balance sheet withstands stress-test scenarios. These financial advantages enable insurers to offer more competitive crediting rates to contract holders. This can lead to higher long-term returns for contract holders and improved profitability for annuity providers.

Index Selection for Annuity Products

The reference index used in MVA calculations is a key design choice, as it is a major component in determining the MVA Amount. Selecting an index that aligns with the insurer’s asset-liability strategy reduces exposure to interest rate mismatches and stabilizes profitability. An index that is highly correlated with the insurer’s assets also mitigates risks tied to early surrenders by preventing surrender values from deviating significantly from their actual asset performance. For example, if the insurer primarily invests in 10-year bonds, the MVA index should be one that tracks 10-year bond yields. Choosing something entirely different, such as 2-year treasuries, would likely not produce an effective formula because the changes in the MVA index would not be a good proxy for the changes in the company’s asset values. The Interstate Insurance Compact defines the MVA “Index” as a “publicly available interest rate index, where the source of the index is external to the company.”

Common Index Choices

- U.S. Treasury Yield Curve – Frequently used for MYGAs, as Treasury rates serve as a standard measure of general market interest rate movements.

- Corporate Bond Indices – Some insurers use corporate bond benchmarks, which better reflect the credit spreads embedded in their investment portfolios.

- Blended Indices – A weighted combination of multiple publicly available interest rate indexes.

- Companies Current Guaranteed Interest Rate (MYGA only) – For MYGAs, insurers are permitted to skip the external index altogether and compare the Crediting Rate from the beginning of the guarantee period with the rate being offered on new MYGA contracts. This methodology allows for a 0.25% pad that increases the Rate at the time of surrender (resulting in a more negative-leaning MVA). The pad allows some relief to insurers offering MYGA for whom crediting rate changes may be a factor of competitive pressure rather than changes in asset value.

MVA Impact on Statutory Reserves

MVAs affect how annuity liabilities are valued on an insurer’s balance sheet, particularly in the calculation of statutory reserves. Statutory reserves are based on prescribed discount rates, which determine the present value of an insurer’s future obligations. Because MVAs reduce disintermediation risk, insurers are allowed to apply a higher discount rate in reserve calculations compared to non-MVA products, leading to lower reserve requirements.

By lowering reserve requirements, MVAs give insurers greater flexibility in product pricing. This efficiency enables insurers to allocate resources more effectively, often leading to more competitive interest rates for contract holders.

Capital Advantages Under RBC C3

Beyond reserves, MVAs also provide capital relief under US Risk-Based Capital (RBC) guidelines, particularly in the C3 component (interest rate risk). The C3 risk charge accounts for potential mismatches between assets and liabilities due to interest rate movements. Since MVAs adjust liabilities to better align with asset values and discourage surrenders in rising rate environments (when insurers would otherwise be forced to sell lower-yielding assets at a loss), the RBC guidelines prescribe lower C3 capital requirements for products that include an MVA. Similar to MVA’s impact on reserving requirements, this reduction in capital strain helps insurers maintain competitive product pricing while ensuring long-term financial stability.

MVA Capstone: Applied Learning

This section presents two perspectives on how Market Value Adjustments (MVAs) evolve under different conditions:

- Single Contract: Tracks the MVA trajectory for a single contract issued five years ago, showing how the MVA fluctuated over time.

- MVA Today for Issues over Previous 5 Years: Shows the MVA as of today for contracts issued daily over the past five years, illustrating how contracts from different issue dates are affected by today’s interest rate environment.

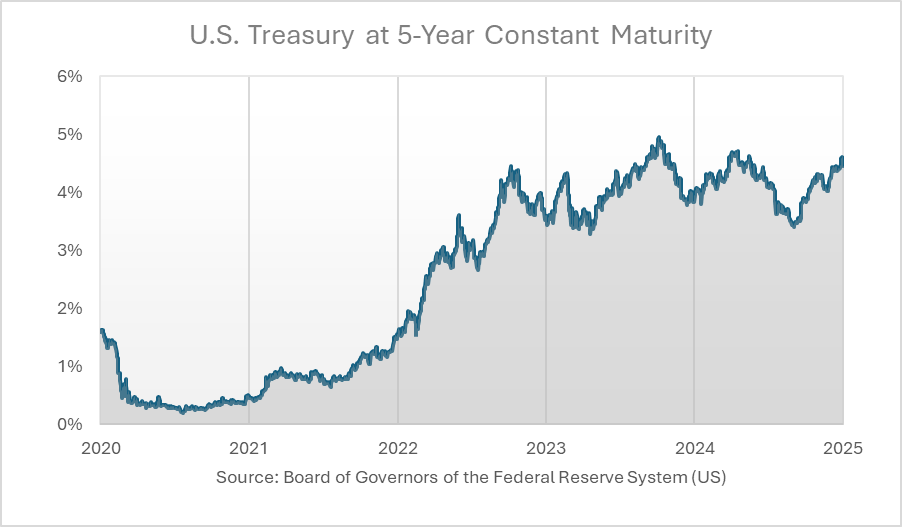

By comparing these perspectives, we highlight how interest rate shifts and time-to-maturity shape the surrender values of annuity contracts. For reference, the chart below shows how interest rates have changed for a 5-Year Constant Maturity Treasury (5-Year CMT) over the past 5 years. This will be the MVA reference rate selected for this analysis.

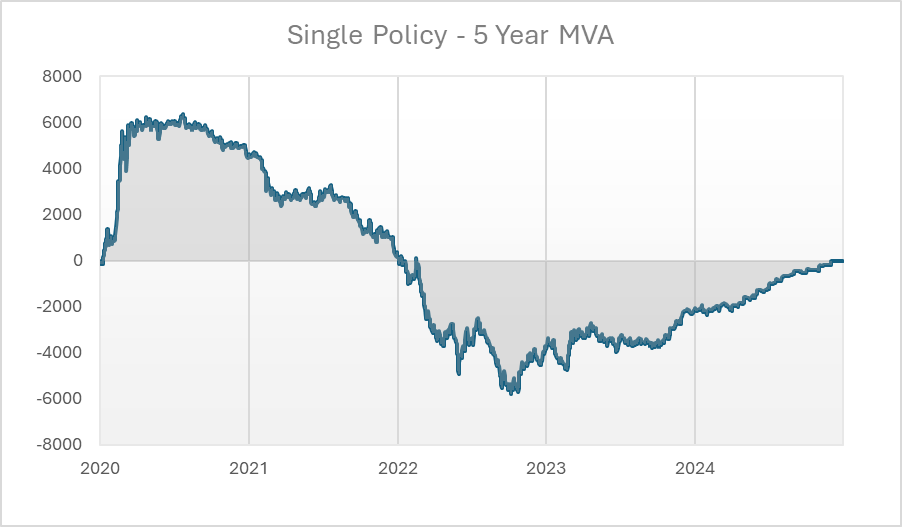

MVA Evolution for a Single Contract Over Five Years

To understand how MVAs change over time for a single contract, we examine a contract issued five years ago and track its MVA year by year.

This hypothetical contract was issued with $100,000 of premium and a 5-year MVA Period. For simplicity, we will assume no account value growth and no limits on the MVA. Here is how the MVA has changed since the contract was issued.

Key Observations

- Early Positive MVA: Right after issue, the 5-year CMT dropped, increasing the value of the insurer’s assets and creating a prolonged period of positive MVA.

- Neutral MVA in 2022: By 2022, the comparison reference rate matched the at-issue rate, resulting in an MVA of zero, as no adjustment was needed.

- Negative MVA Takes Hold: From 2022 onward, rising rates reduced the value of at-issue assets, leading to a negative MVA and lowering the contract’s surrender value.

- MVA Impact Fades Over Time: As the tracked asset nears maturity, the MVA period shortens, naturally decreasing the magnitude of the MVA.

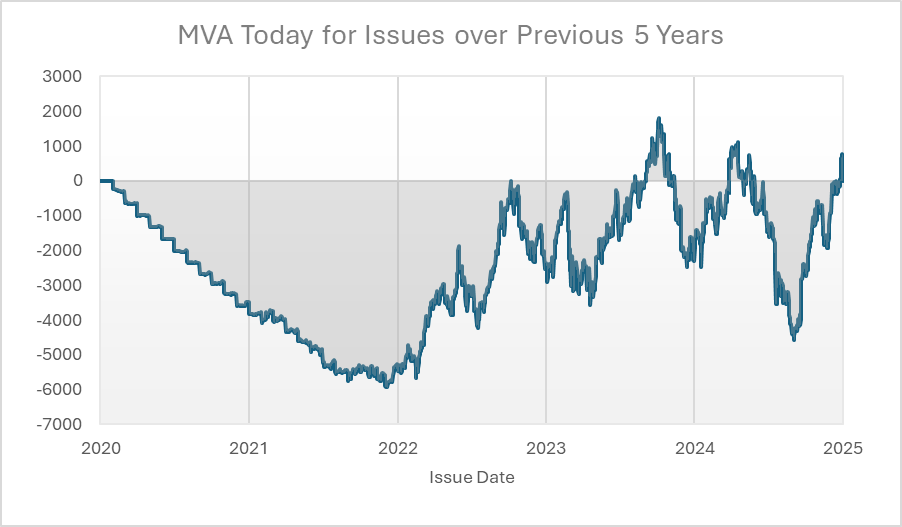

MVA Snapshot for Contracts Issued Over the Last 5 Years

Unlike Chart 1, which examines a single contract over time, this chart captures the MVA for contracts issued on different dates but evaluated on the same day. This offers insight into how historical rate environments affect surrender values today.

The hypothetical contracts in this chart represent a contract issued on each day for the past 5 years. Assume $100,000 of premium, a 5-year MVA Period and no-account value growth. Here is the MVA value today for each Contract.

Key Observations

- Older Contracts Face the Largest Negative MVA: Contracts issued in low-rate years (2020-2021) have the most negative MVAs today, as their assets are worth less in the current higher-rate environment. Notice the stair stepping nature of the line, this is because N is based on Months to expiration and rises in this example at the end of each month.

- Mid-Cycle Contracts Hit a Tipping Point: Contracts from Years 3-4 show smaller or neutral MVAs since the rate at issue and today’s comparison rate are more aligned.

- Recent Contracts See Minimal Impact: Contracts issued recently were priced in today’s interest rate environment and the change in the MVA Reference Rate is comparatively less; however these contracts are further from maturity and are subject to more volatile swings due the N factor.

Summary

Market Value Adjustments (MVAs) are a critical feature in annuity pricing, aligning surrender values with market conditions to create fair and sustainable outcomes for both the client and the insurer. Rather than acting as a penalty, MVAs protect insurers from financial losses due to early withdrawals, allowing them to offer higher credited rates.

For clients, MVAs ensure a more equitable system by preventing early surrenders from negatively impacting those who stay invested. Without an MVA, insurers might be forced to sell assets at a loss, which could reduce credited rates for all contract holders. While negative MVAs can lower surrender values in rising rate environments, they ultimately preserve contract value and protect long-term contract holders from bearing the cost of market fluctuations.

From an industry perspective, rate volatility makes MVAs essential in product design. Insurers must manage risk effectively, while advisors play a key role in ensuring consumers understand how MVAs function.

Regulators prioritize protecting contract holders and ensuring insurers can meet their long-term commitments. MVAs support this objective by mitigating interest rate risk, increasing the likelihood that insurers can fulfill their contractual obligations. By adjusting surrender values based on market conditions, MVAs promote financial stability and fairness across all contract holders.

As interest rates fluctuate, MVAs will remain a necessary tool in annuity pricing. Transparency and education will be key to reinforcing their value in the marketplace.