Week in Review – 5/8/2026

Product Updates

Knighthead Charts a New Course

After establishing itself as a serious newcomer in the MYGA market, Charlotte, NC-based Knighthead Life is heading in a new direction. Earlier this week, the AM Best A- rated carrier launched two new FIAs—the first indexed-linked products in its annuity lineup. Chartline and Chartline Bonus join Knighthead’s Staysail MYGA as accumulation-focused products that offer principal protection. The FIAs will look to build on the success of their Staysail sibling, which has routinely sat near the top of the competitive leaderboard since its launch.

Like any new entrant, Knighthead is about to learn that the competitive calculus is a different animal in the FIA market. While comparing MYGAs to each other is relatively straightforward, FIAs have many more moving parts that make apples-to-apples comparisons almost impossible. Unique crediting methods, engineered indices, and all kinds of supplementary features are commonplace among FIAs and are at the heart of product differentiation. To succeed, Knighthead’s Chartline and Chartline Bonus will need to thread the needle between keeping things simple and leaning on uniqueness to stand out among the crowd.

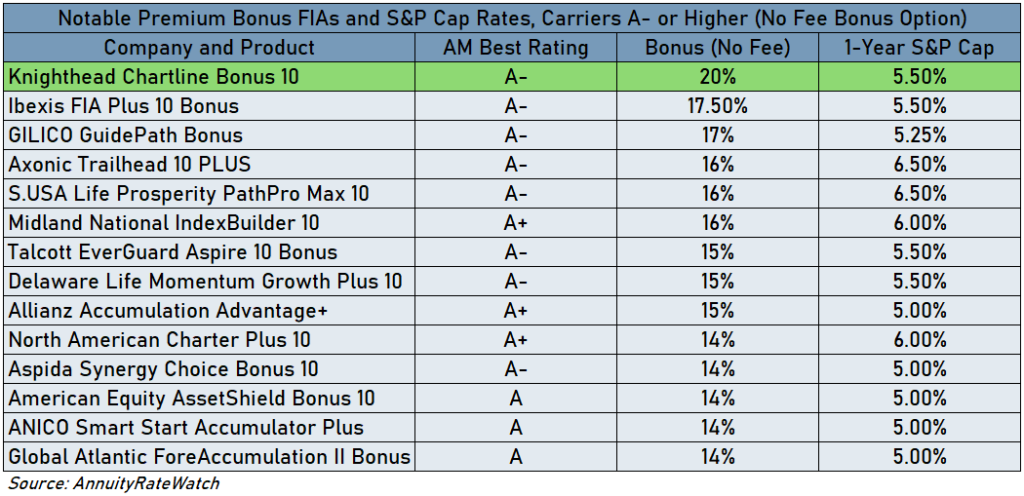

What’s a simple way to set yourself apart from your peers? By offering the largest upfront premium bonus—for no additional fee. The new Chartline Bonus FIA completely resets the bonus market among A- or higher rated carriers with a 20% no-fee premium bonus available on the 10-year version of the product up to age 75. Prior to the launch of Chartline Bonus, Ibexis held the top spot with a 17.50% bonus on its FIA Plus 10 with Premium Bonus product. Perhaps most impressively? Chartline Bonus does not sacrifice upside potential to offset such a strong bonus.

An S&P 500 cap of 5.50% matches or exceeds the cap offered within similar products, including those with the next largest bonuses from Ibexis and GILICO, as well as notable products from Athene, Delaware Life, Aspida, and American Equity. Knighthead’s aggressive leap to the top of the bonus space will certainly draw the attention of producers and consumers looking to exchange old, underperforming contracts into new ones with premium bonuses that more than offset any residual early termination charges.

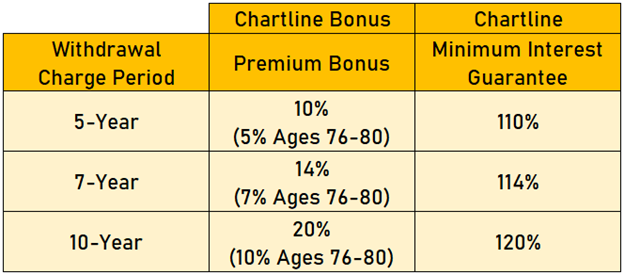

Complementing the upfront premium bonus of Chartline Bonus is the Minimum Interest Guarantee feature automatically included with the non-bonus Chartline FIA. In a layout that is symmetrical to the structure of the Chartline Bonus FIA, the Minimum Interest Guarantee feature on Chartline offers a 2%-simple-interest-per-year backstop for those concerned about the worst-case scenario of purchasing a FIA, for no additional charge. For any consumer with a contract value below the benefit base at the end of the withdrawal charge period, Chartline will “true up” the contract value to match the benefit base. Gone are the days of the “zero is your hero” sales adage with Chartline and Chartline Bonus. Each product guarantees some form of contract value growth for those who keep their contract in force for the duration of the withdrawal charge period.

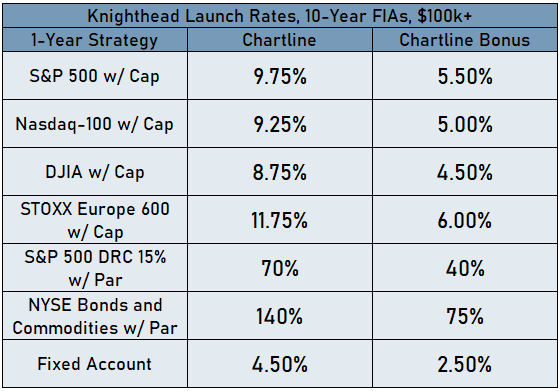

If the premium bonus is the headliner of the product launch, the available crediting strategies coalesce into a strong supporting act. In addition to a fixed rate strategy, Chartline and Chartline Bonus offer a concise yet robust lineup of six indexed strategies, each based on a different underlying index. While six indices may sound like a lot for a new product, many of them are well-known. Among them is the Dow Jones Industrial Average (DJIA), one of the most recognizable indices in the world which, as of the May 4, 2026 launch date, did not appear in any other FIA on the market, according to AnnuityRateWatch. (Earlier this month, Jackson received approval to include the index in its next RILA iteration.)

Knighthead was undoubtedly excited to claim itself as the sole provider of the index in an FIA. This was true at the time of launch, but it was a remarkably short-lived title: coincidentally—or maybe not—American Equity added the DJIA to its lineup just two days later. This may feel like a downer for Knighthead, but does it threaten Chartline’s differentiation story? Hardly. The highest cap on DJIA in AEL’s product suite is only 7.00%—well off the 8.75% available for full allocation in the 10-year version of Chartline. This amounts to a difference in option cost of about 0.80%.

Notably, four of the six indices found in Chartline and Chartline Bonus do not have a volatility target. Of the two that do, one of them—S&P 500 Daily Risk Control 15%—has live performance dating back to 2009. For those with engineered index fatigue, Knighthead’s lineup is sure to be a welcome breath of fresh air. None of the caps or participation rates stand out as absurdly competitive as ones from other recent entrants have, but they seem to put Knighthead in a position to compete.

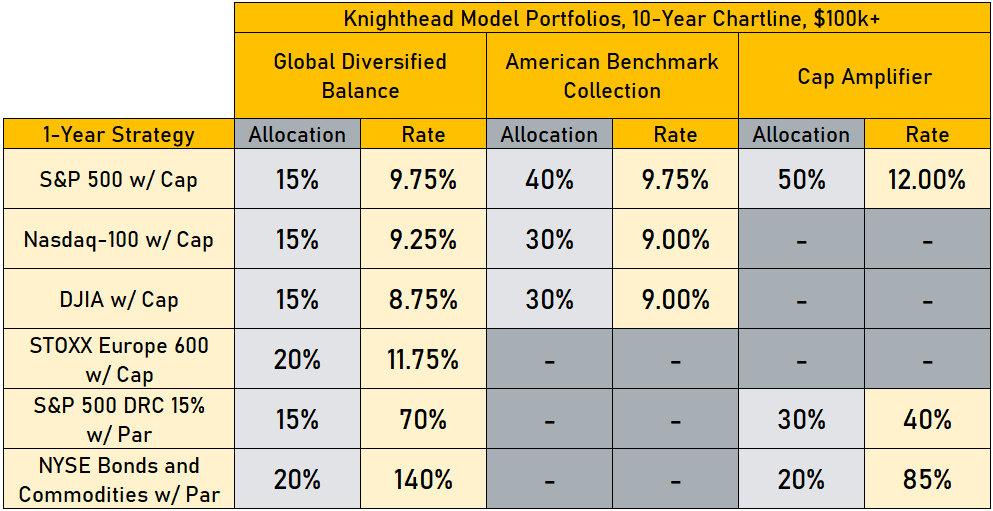

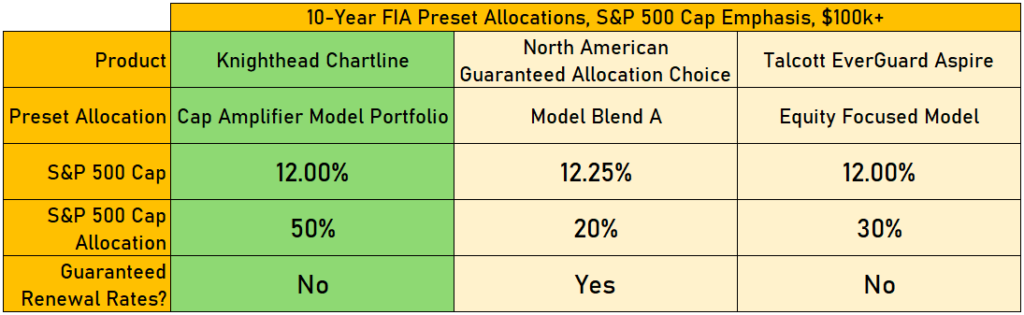

Elsewhere on the rate sheet, the new FIAs put Knighthead among the list of carriers offering preset allocations to consumers within their products. American National, Americo, Athene, Delaware Life, North American, and Talcott all offer these options, with structures varying from simple check-the-box diversification strategies to designs intended to match the consumer’s risk appetite. Chartline and Chartline Bonus offer three preset allocations: the Global Diversified Balance Model Portfolio, the American Benchmark Collection Model Portfolio, and the Cap Amplifier Model Portfolio.

The Global Diversified Balance model spreads allocations out relatively evenly among all six indexed strategies. The rates offered within the model match those available for manual selection, indicating that the model is for those looking for check-the-box diversification simplicity. The American Benchmark Collection model centers on the three most recognizable domestic market indices and leaves out volatility control concepts entirely. Ardent supporters of simplicity within indexed annuities will be hard pressed to find an allocation story as simple and compelling. While the rates in the model are similar to those available outside of the model, they are slightly different. The Nasdaq-100 cap is 0.25% lower in the model and the DJIA cap is 0.25% higher—aligning them at the same cap level.

The third and final preset allocation, the Cap Amplifier model, does exactly what the name suggests. In exchange for lower participation rates on the S&P 500 Daily Risk Control 15% and NYSE Bonds and Commodities indices, the 50% allocation to the S&P 500 cap strategy comes with a more attractive cap. It’s blatant cap subsidization—but it’s not trying to hide the fact that it is. Unlike several carriers that subsidize S&P 500 caps, Knighthead is doing it more transparently within the confines of the model. From a pricing perspective, subsidizing within a model allows Knighthead to price the amplified cap with allocation certainty. The model stacks up against similar ones offered by North American and Talcott that do not lower rates on other strategies but enforce stricter limits on the S&P 500 cap allocation.

The launch of Chartline and Chartline Bonus is an ambitious next step for Knighthead, a carrier seeking to expand its footprint in the annuity market. The refusal to entirely sell out and join others in the subsidization game outside of the Cap Amplifier model is unique, and that comes with risk. The common denominator among FIAs is the S&P 500 cap strategy, the most allocated-to option in the industry. It is seen as the key indicator of a FIA’s general competitiveness—fairly or not. So, for a carrier as competitive in the MYGA market as Knighthead has been in the last year plus, it is somewhat surprising to see the S&P 500 cap outside of the model portfolios below 10.00%. As of this writing, at least ten other carriers meet or exceed that mark. Maybe that’s an intentional effort to ensure sustainable renewal rates and direct more attention to the model portfolios (Cap Amplifier, specifically) for those looking for the highest cap.

With an ultra-competitive premium bonus and ample mix of well-known indices in individual strategies and model portfolios, Knighthead’s FIAs seemingly have multiple avenues to win business in the accumulation-focused FIA market without relying purely on the S&P 500 cap. Will it pay off? Knighthead has set its new course. Now comes the harder task—convincing distribution partners that it’s a journey worth taking. -Jon Blomquist

Guaranteed Income Snapshot – May 2026

After last month’s detour into 2025’s top-selling guaranteed income carriers, we’re back to a typical guaranteed income review. This month delivered two notable income rider updates from F&G and Global Atlantic. F&G was featured as the fourth-highest selling carrier in last month’s article, so any change they make is worth keeping an eye on.

Notable Updates & Callouts

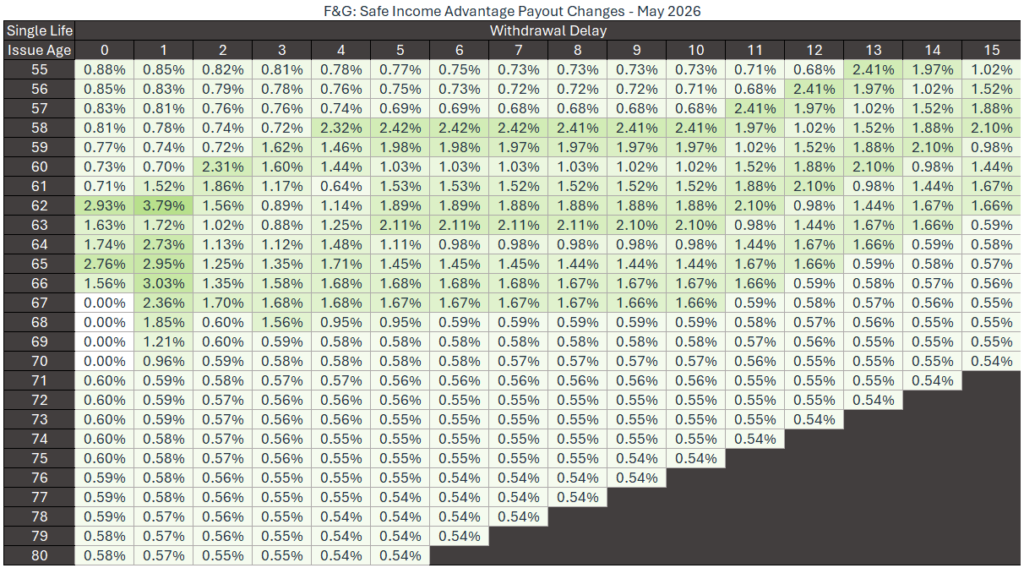

F&G: Safe Income Advantage – Safe Income Advantage got a payout rate bump this month. It’s a modest lift, but worth noting as the last update to this product was back in September 2025. Given Safe Income Advantage’s strong sales and market position, there’s not much pressure to tinker with it more often.

Here is the full scope of payout changes (% increase from previous month):

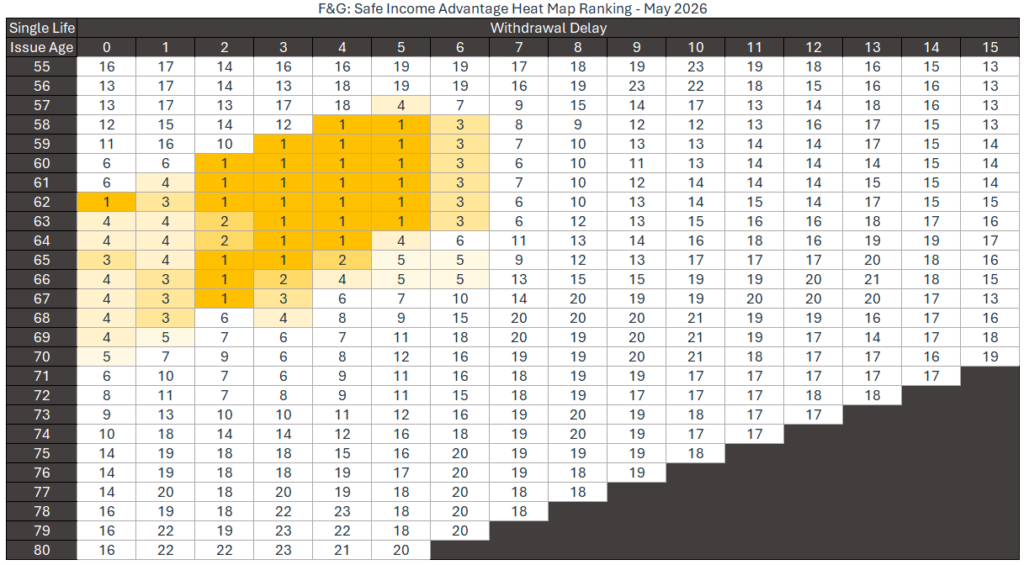

And here’s how it looks on a competitive heat map:

F&G does not dominate every cell in our guaranteed income snapshot because we only look at a few targeted categories. But we can see from the heat map above that F&G is the most competitive product for income ages 62-69 when deferrals are five years or less. F&G offers a strong spread of top offerings over a modest region of income ages.

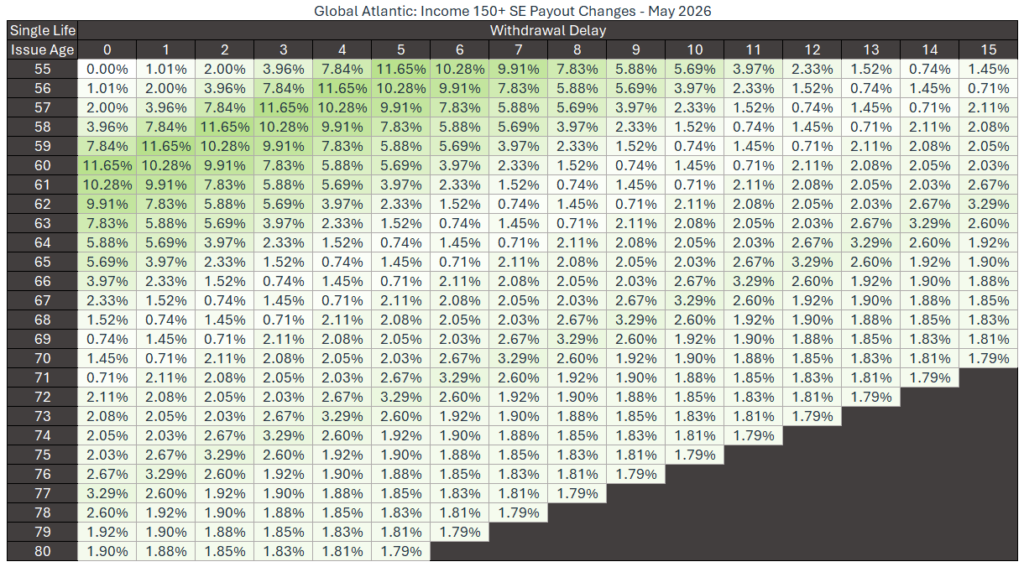

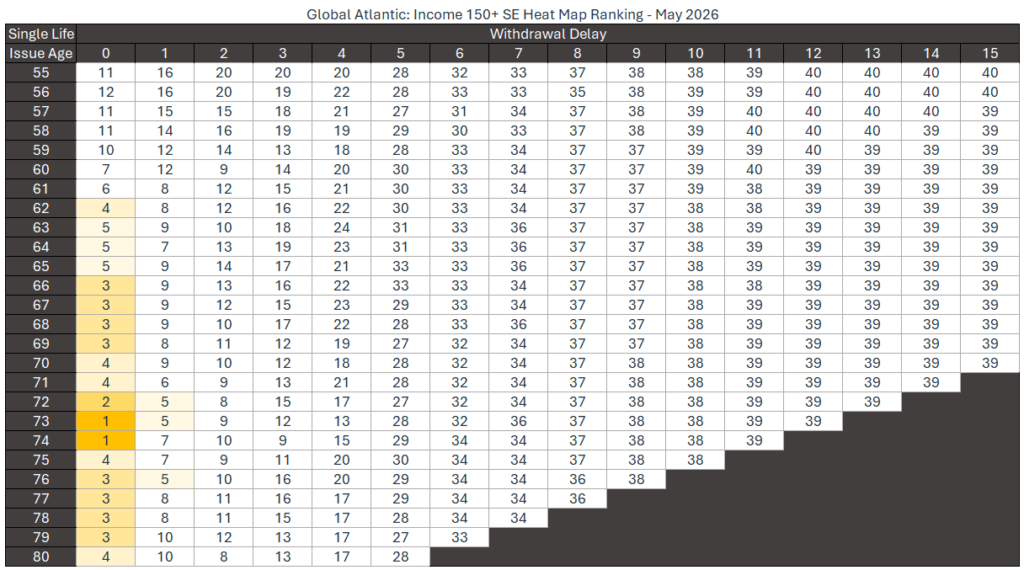

Global Atlantic: Income 150+ SE – Global Atlantic also pushed payout rates higher this month, boosting Income 150+ SE payouts across its full range of income options. The last update was back in April 2025, so this seems like an annual refresh. Historically, this product has been most competitive at high issue ages with immediate income. Let’s see if this still holds true today.

Here is the full scope of payout changes (% increase from previous month):

And here’s how it looks on the competitive heat map:

Yep, still true. Consistent with their past performance, this product remains primarily competitive when electing immediate income. Global Atlantic follows a common market trend of payouts peaking in a few cells with a significant drop-off the farther you get from that location. Income 150+ SE saw a slight boost to payouts in their competitive region, with most of their larger payout increases focused on younger income ages. We took a deeper look at this product change last week, with a more detailed review of Global Atlantic’s guaranteed income change.

No other products were updated by carriers this month. For context, here’s the full menu of items that carriers can update when making product changes (common ones in bold):

- Payout rates

- payout rate structure (1-dimensional vs 2-dimensional)

- Rollup rate

- Rollup rate type (simple vs compound)

- Benefit base bonus

- Benefit base bonus rollup type (simple vs compound)

There are other bonuses and features unique to specific products, but these options cover the majority of the market. This month was purely a payout rate story, but we’ve seen all these items adjusted at various points. We’ll keep watching to see whether any carriers respond to F&G and Global Atlantic’s moves.

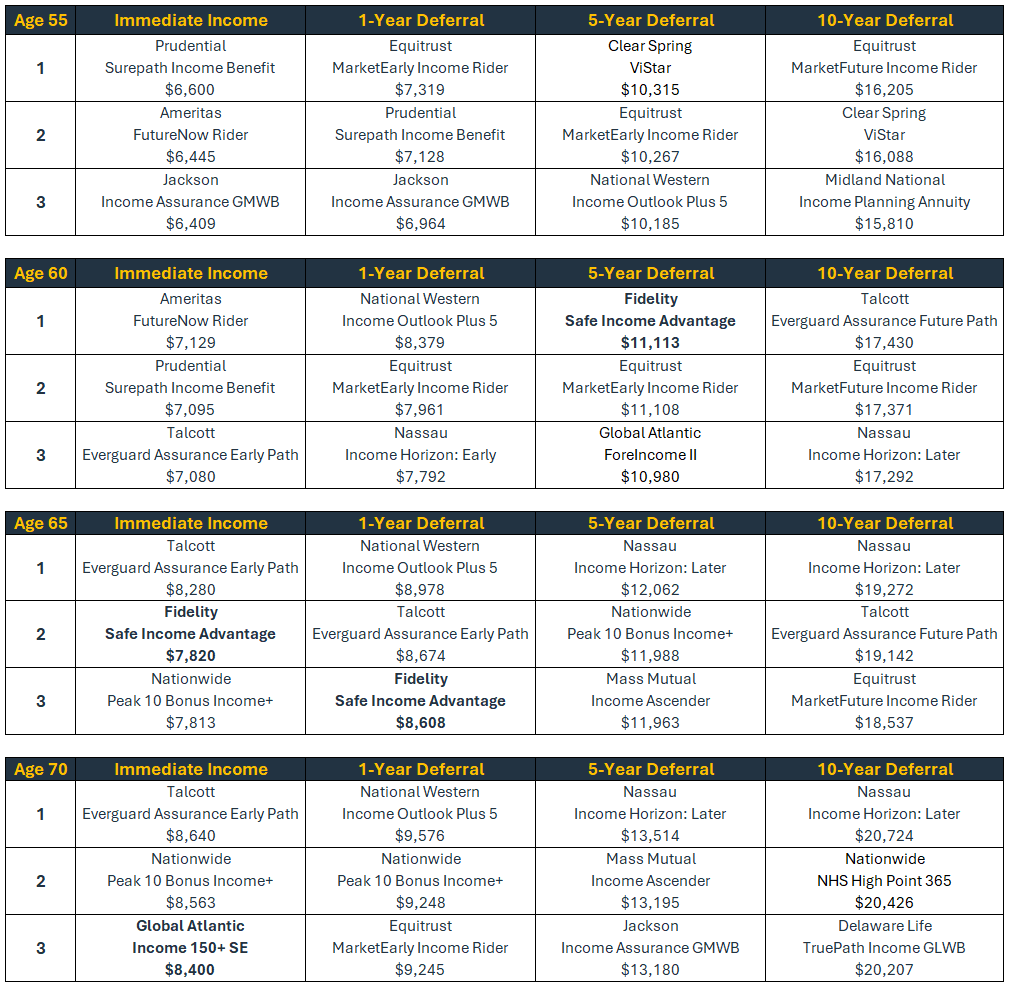

For the standings, we look at commissionable FIA products that are sold primarily in the IMO channel. We only include the top products for each carrier that fit this profile. Bolded products either have seen changes to their payouts or are new to the competitive standings compared to the previous month. Below are the Top 3 products and guaranteed income amounts for multiple age ranges and deferral periods:

See you next month. -Caleb Shumpert

Filing Updates

The Float Is Back – No Cap!

In 2016, Security Benefit launched its RateTrack product, a MYGA with a fixed and floating rate component. Analysts anticipated that copycats would follow quickly afterwards, but instead, the market nearly had to wait a full decade. CL Life, a B++ rated carrier, made a brief attempt in 2024 with a SOFR-based floating rate annuity called High Trestle, but it never gained any traction and has since been pulled from their product lineup. Now, Oceanview, backed by a considerably larger distribution engine, has become the first serious competitor to enter the space with their recently approved filing with the name CurrentRate. The filing hints at a similar chassis to RateTrack – a fixed base rate plus an annually resetting float rate – but also a few meaningful differences.

The CurrentRate product is filed as a single-premium deferred annuity and leans on a flexible filing to potentially offer a rate guarantee period anywhere from 2 to 12 years with a matching withdrawal charge period duration. Oceanview’s existing MYGAs, Harbourview and Sky Harbourview, offer 2 to 7-year guarantees and 3/5/7/10-year guarantees respectively. For CurrentRate, the annual interest to be earned on the premium is the sum of the Guarantee Period Base Rate that is locked for the duration of the guarantee period, plus a Floating Rate Component that is equal to the average of the last 10 business days of the 1-year US Constant Maturity Treasury rate prior to the contract’s anniversary. Notably, the filing also includes flexibility to switch the benchmark of the crediting rate to SOFR in the future. An MVA rider is attached automatically, whereas RateTrack does not include an MVA, and a 10% free withdrawal rider will kick in after the first year. The MVA will adjust the surrender value of the contract up or down based on the difference between the contract’s credited rate and the rate currently being offered on new issues for the same guarantee period. In a rising rate environment, the MVA would reduce the surrender value and partially offset the benefit of a higher crediting rate for owners who exit early. While an MVA is present on nearly every MYGA and FIA in the industry, most base the adjustment on an external benchmark, such as treasury rates. The CurrentRate filing takes a different approach and bases the adjustment on the current crediting rate that Oceanview is offering to new issues.

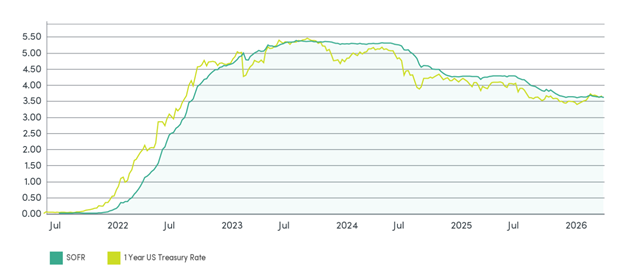

Interestingly, the filing does not mention anywhere that the Floating Rate Component is capped. If that is the case, when the 1-year US CMT rises, this product will be able to offer substantially higher crediting rates as a result. The uncapped floating rate component tied to the 1-year CMT is the main differentiator that can help set the new product apart from RateTrack’s capped floating rate component based on the 3 Month CME Term SOFR Reference Rate. The 1-year CMT is a forward-looking rate based on where the market thinks interest rates are going, while the 3 Month SOFR captures what has been happening in the overnight Treasury markets – almost like looking in a rearview mirror. The graph from Security Benefit below shows a comparison of the two different products’ floating component reference rates. There are a few things that jump out: First, you can see that the SOFR was higher than the 1-year US Treasury Rate from late 2023 until early 2026, with the 1-year CMT being either equal or slightly higher so far this year, and second, the SOFR curve looks very similar to the CMT curve, just shifted or delayed by a couple of months. In the rising interest rate environment that began in late 2021, the 1-year Treasury Rate was much quicker to react, giving it nearly a 100 basis point head start on SOFR. If rates move again and that gap makes another appearance, CurrentRate’s uncapped structure would see the bump immediately.

The uncapped floating rate component raises an interesting question about how Oceanview plans to manage that exposure. The typical hedge for a floating rate liability is a pay-fixed, receive-floating interest rate swap, where Oceanview would receive the 1-year CMT rate from another party while paying a fixed rate funded by the product’s asset yield. This would allow Oceanview to offset what they are crediting policyholders as part of the Floating Rate Component and mitigate their exposure to interest rate fluctuations.

That hedging question aside, the competitive opportunity that Oceanview is stepping into is hard to ignore. After RateTrack launched in 2016, the product saw immediate success, with over $1 billion of sales in each of the first two years, according to Beacon. Sales have slowed as both the interest rate environment and RateTrack’s floating rate benchmark (originally LIBOR) have changed. In 2025, the product’s annual premium dipped to under $14 million. Oceanview is diving into the floating rate MYGA market at a time when the market is wide open.

Oceanview sold over $2 billion worth of their Harbourview and Sky Harbourview MYGAs in 2025 (Beacon). Will CurrentRate be able to add to that number? Until the product launches, keep an eye on the 1-year CMT rate for a preview of where the Floating Rate Component lands and watch for the rate sheet to see how aggressively Oceanview prices the base rate alongside it. -Jayden Juergensen

Benchmarks

Fair-Market S&P 500 Caps and Participation Rates

| Date | Option Budget | S&P 500 Cap Rate | S&P Par Rate |

| 5/8/2026 | 5.02% | 9.69% | 59.62% |

| 5/1/2026 | 5.11% | 9.74% | 59.62% |

| 4/24/2026 | 4.99% | 9.35% | 57.57% |

| 4/17/2026 | 4.96% | 9.28% | 57.71% |

| 4/10/2026 | 5.02% | 9.23% | 57.42% |

| 4/3/2026 | 5.08% | 9.40% | 54.05% |

| 3/27/2026 | 5.09% | 9.38% | 51.86% |

| 3/20/2026 | 5.11% | 9.47% | 54.20% |

| 3/13/2026 | 5.05% | 9.35% | 54.05% |

YTD Index Returns as of 5/7:

- S&P 500: 7.18%

- Nasdaq: 13.13%

- Dow Jones: 3.19%

Treasury Yields (week over week change, as of 5/7)

1-year: 3.76% (+4 bps)

2-year: 3.92% (+4 bps)

3-year: 3.94% (+3 bps)

5-year: 4.04% (+2 bps)

10-year: 4.41% (+1 bps)

20-year: 4.96% (-1 bps)

30-year: 4.97% (-1 bps)