Week In Review – 3/13/2026

Product Updates

Cleared for Takeoff: Athene’s Aviator FIA

Earlier this week, the industry’s number-one seller of indexed annuities announced the launch of their newest indexed product, Athene Aviator. Offered in 5-year and 10-year variants, the product joins a robust lineup of FIAs on Athene’s shelf, which is headlined by the income-oriented Ascent Pro and the accumulation-oriented Performance Elite. Aviator, the latest FIA that Athene hopes to see fly high in the IMO channel, looks to capitalize on a mantra the industry has been hearing incessantly from distributors, advisors, and consumers: keep it simple. Titled “ASPR” in the then-pending Florida filing we covered back in November, the cryptic acronym may have stood for “A Simple Product, Really.”

Aviator’s rate sheet simplicity will be one of its calling cards. The product has no optional riders, no fees, and no premium bonuses. It is singularly focused on offering accumulation potential through crediting strategy optionality. The rate sheet offers consumer choices but keeps the conversation straightforward and crediting rates incredibly consistent.

The Diversified Blend Strategy (DBS) is essentially a contractual model portfolio, allocating premium across each of the three engineered indices with a constant participation rate. The calculation of the index-linked interest earned in a DBS occurs independently for each of the three indices—flooring the return of each at zero—before adding them together as the interest earned for the DBS itself. Athene’s “Strategy Preset” allocation options are also available with Aviator but cannot be used in conjunction with DBS. Strategy Preset allocates premium among separate strategies according to weights governed by each of the Conservative, Balanced, or Growth options. They’re similar, simple methods for a consumer to diversify premium allocations within their contract. Athene markets the differences by describing DBS as a “manual flight path” and Strategy Preset as an “autopilot path” in a smart play-on-words with the Aviator name.

Another observation from the Aviator rate sheet? The prominence of Bank of America’s patented Fast Convergence intraday volatility methodology. It forms the backbone of each engineered index’s rebalancing structure and builds on a story that is well-known by many distributors familiar with the rest of the Athene product portfolio. The 7% volatility target on each index seems low in today’s rate environment—especially on the equity-focused S&P 500 FC and Invesco QQQ FC options—but they will help keep participation rates more attractive in future, potentially lower rate environments. It’s worth wondering whether the low volatility target will be received well by Athene’s distribution partners.

With “FC” on each of the three engineered indices, expect that Bank of America will fully hedge that portion of the business. This type of arrangement likely makes it easier for Athene to offer level participation rates among each index across crediting terms. While we cannot know for sure, we imagine that this sort of pricing synergy among the three indices was a key reason for Athene cutting existing index partners out of the Aviator product. BNP Paribas, HSBC, and UBS each have engineered indices within Athene’s other FIAs and would have certainly liked to be part of the newest product from the top FIA seller in the market. The most notable omission is certainly BNPP’s MAD 5, a multi-asset index which just celebrated its 10th anniversary of live performance.

Outside of the rate sheet, things get more complex. Sure, there is no optional income rider, no gaudy premium bonus, no rate buy-up strategies, and no other charge-based features. But Aviator brings complexity to a product category that has typically been measured in point-to-point increments. Their “Strategy Daily Value” is a RILA-like interim value that quantifies the value of funds in the strategy based on the current index value and applicable crediting rates. The formulas describing the calculation employ many “if this, then this” type of statements aimed at carving out all possible scenarios and preventing Athene from being on the wrong side of an unwinding hedge.

Notably, this does not produce a “true” interim value like we see on RILAs. Since this methodology is not based on a market valuation of the underlying options, there is a larger risk of mismatch. Because of that risk, the Strategy Daily Value is set up to be worth less than the “true” interim value would be. Does it still provide a mid-term strategy value more favorable than nearly all FIAs in the market that lock the strategy value until the end of the crediting term? Absolutely. But as we discovered in the review of the filing late last year, any gains from mid-term performance only apply to the free portion of the strategy value—an important detail that will surely be glossed over in the feature’s elevator pitch.

Another mid-term feature found in the product is the “Index Lock” option, which provides consumers the ability to lock in the current value of an index within a crediting strategy, effectively locking their end-of-term interest credit. This type of control combats fears related to sequence of returns and gives consumers an additional lever to pull if they choose. Will distributors in the IMO channel be as likely to pitch clients on the Index Lock feature as registered representatives are with performance locking on RILAs? Some certainly will. But others, understandably, may shudder at the thought of all the “Do you think I should lock today?” questions their client base will be sending their way.

The “Index Lock” feature will only be available on strategies with uncapped participation rates, based on both their filed contract schedule page (which coincidentally lists the same 9.50% in the final row as the S&P cap debuting on the 10-year version of the product) and the nature of option pricing dynamics. On an uncapped participation rate strategy, locking the index value mid-term forfeits upside and downside potential throughout the rest of the term. On a capped strategy, a consumer could theoretically lock and only forfeit the downside if the index value is above the threshold needed to earn the cap. In this scenario, the market value of the options held to replicate the payoff would be less than the intrinsic value the consumer is locking in, exposing Athene to potential losses. This risk is one that Athene will avoid, so expect Index Lock to only be available on uncapped participation rate strategies.

Athene positions both Index Lock and Strategy Daily Value as features aimed at providing transparency to the product—and they do, to a point. But transparency into complexity can just as easily invite more questions than it answers. Whether those questions materialize or not, it would be foolish to bet against Athene’s ability to position Aviator effectively with their distribution partners. They didn’t become the top seller of indexed annuities by accident. Expect sales—fueled by Athene’s momentum and reputation—to take off in 2026. The only question is: how high will Aviator fly? -Jon Blomquist

Allianz’s New Choose-Your-Own-Adventure RILA

In an effort to improve upon the success of Index Advantage+ Income Variable Annuity, its popular income-focused RILA, Allianz Life introduced Index Advantage+ Select Income Annuity earlier this week. The launch comes days after Q4 2025 sales results indicated the Minneapolis-based carrier pulled off a 17% year-over-year increase in RILA sales to maintain its 2nd-place standing in that corner of the market.

Allianz has a reputation for being on the leading edge of product innovation, particularly in the RILA space. The arc of their product development efforts often have a theme of increased policyholder flexibility and choice, and Index Advantage+ Select Income is no exception. But before we get into what’s new in Select, let’s review the core mechanics of the existing product.

Index Advantage+ Income is a RILA chassis that features an automatically embedded GLWB rider with the very creative name of “Income Benefit”. Like all of Allianz’s income-oriented offerings, the product is focused on upside potential – the minimum guaranteed income is modest, but it can grow based on the performance of the underlying contract value. There is no concept of a separately-tracked benefit base, guaranteed roll-ups, or anything of that nature; the income amount is simply the contract value multiplied by an Income Percentage. The Income Percentage is determined on the income start date based on the policyholder’s attained age and the number of years income was deferred.

On the income start date, which must be a contract anniversary, the policyholder can elect either “Level Income” or “Increasing Income”. The name of the Level option arguably undersells itself: once income begins, it can automatically increase on each anniversary if the contract value is greater than it was on the previous anniversary. In other words, if the contract value growth outpaces withdrawals and charges, income can increase, otherwise it remains level. The Increasing Income option takes this a step further and applies an increase to the income amount any time the interest credited to the underlying index options is positive, regardless of whether it exceeds the drag from withdrawals and charges. The way this is accomplished mechanically is by reallocating the entire contract value among 1-year, zero-floor index options on the income start date. Being a RILA, many other allocation options are available before income begins, but in the income phase, only the fully protected options are available to ensure that the income amount cannot decrease year-over-year.

IA+ Select Income and its embedded “Income Benefit II” rider introduce a couple new features that give policyholders greater flexibility. Instead of requiring income to begin on the anniversary, Income Benefit II allows this election to occur on any date, outside of the 14-day window leading up to an anniversary. More significantly, the Increasing Income option is replaced with a Dynamic Income option. With the Dynamic option, income can decrease year-over-year, allowing for greater potential upside – the fundamental value prop of a RILA itself. Mechanically, the calculations are the same between the two – the annual income amount changes by the same percentage as the underlying index options each year. The only difference is that the Dynamic option allows allocation to any one-year index option, not just those with full downside protection. Think of it this way: Increasing Income is to Dynamic Income as FIA is to RILA.

This opens up quite a few additional choices for policyholders to dial in their desired risk/reward tradeoff. The “Performance” strategy offers a 10%, 20%, or 30% buffer on losses with a cap on the upside. The “Dual Precision” strategy has the same buffer levels, but with a trigger rate that applies as long as the index doesn’t breach the buffer. The standard “Precision” strategy comes with a 10% buffer, but only pays the (higher) trigger rate if index performance is greater than zero. The “Guard” strategy has a -10% floor with a cap. And the fully-protected options (“Protection” strategy) remain available, with either a cap or trigger on the upside. Any of the above crediting strategies can be paired with one of the five indices offered in the product: S&P 500, Russell 2000, Nasdaq-100, iShares MSCI Emerging Markets ETF, or EURO STOXX 50, for a total of 50 unique index options. And those are just the one-year options. Before income begins, policyholders also have access to 3- and 6-year versions of 12 of those 50, which brings the number of pre-income options to 74.

How do these differ from IA+ Income’s lineup, you ask? Surprisingly, not at all. Not only is the list of available options the same, but the rates themselves are identical. In fact, even the Income Percentages for the Income Benefit II rider are identical to the corresponding rates in the existing Income Benefit rider. Rider fees, surrender charges, free withdrawal provisions… all exactly the same. This begs the question: why did Allianz bother to roll this out as an entirely new product? The Dynamic Income option is cool and all, but surely they could’ve brought it to market in a simpler way, like adding an additional GLWB rider option within IA+ Income. Why a whole new product? And furthermore, why an additional product? Keep in mind, IA+ Income is still available alongside its new sibling.

We don’t know for sure, but there is one other tiny difference between the two that might hint at Allianz’s master plan. If you pay very close attention to the marketing names, you’ll notice that there’s one word that’s present in all of their existing RILAs but is suddenly missing from this new product: “Variable.” Every other product name ends with “Variable Annuity”; this one just ends with “Annuity.” If there’s anything we know about the Allianz crew, it’s that they pay meticulous attention to detail, which makes us doubt this was an accident. IA+ Select Income is still very much a RILA, and omitting the word “Variable” from the name will not exempt it from regulatory classification as a type of variable annuity. But this subtle rebrand might indicate Allianz is making more of an effort to expand distribution beyond the traditional VA advisors that have been the primary sellers of RILAs to date. As we noted when we covered Athene’s forthcoming RILA, few have had success doing so thus far. Will both income products stay on the shelf long-term? Or will IA+ Income eventually pass the torch to IA+ Select Income and ride off into the sunset? It remains to be seen, and likely depends on how well the idea of decreasing income risk is received by the market. If it works, expect to see Allianz close the gap that Equitable holds in the top spot on the RILA sales charts. If it doesn’t, you can bet they’ll be back with another industry-first idea soon enough. -Drew Schmalz

Guaranteed Income Snapshot – March 2026

St. Patrick’s Day is almost here, and while lucky charms are hard to come by, guaranteed income doesn’t have to be. While our guaranteed income leaderboard did not see a lot of change after February’s big shakeup, product activity was higher than usual this month. Eight different carriers made product adjustments to their GLWB riders, as average payouts continue to increase across the industry.

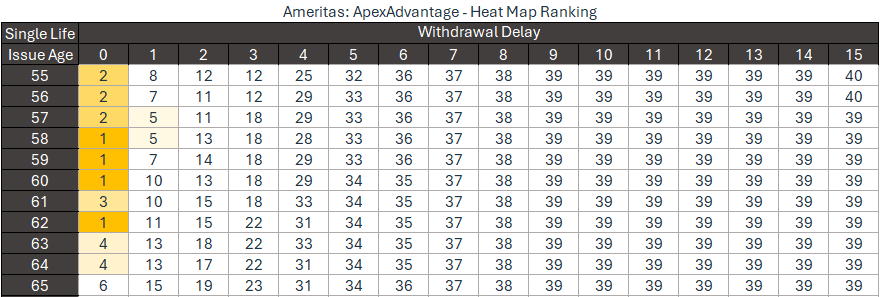

The most substantial move we see this month is Ameritas with ApexAdvantage, jumping up in the immediate income rankings. This product has not offered competitive payouts since at least 2024, making its debut in the rankings this month. When looking at the GLWB rider, Ameritas is clearly targeting early income with a 34% rider bonus, 5% compound rollup for only three years, and payout rates that don’t increase after that third year across most issue ages. This is the most targeted income product on the market right now, as the competitive heat map below makes clear. ApexAdvantage is fully intended as immediate income, with no intention of offering any other alternative.

Midland National with Income Planning Annuity returns to third on our competitive rankings in the 55-year-old, 10-year-deferral bucket, boosted by their recently increased Lifetime Payment Percentages. The last time we saw Midland National was in June 2025, but this monthly update elevates Income Planning Annuity payouts past their previous levels. This rider is designed to be more competitive the longer income is deferred, with 10 years being the optimal position. Waiting each additional birthday after issue increases the lifetime payment amount by 10% for the first 10 years, dropping to 2% thereafter.

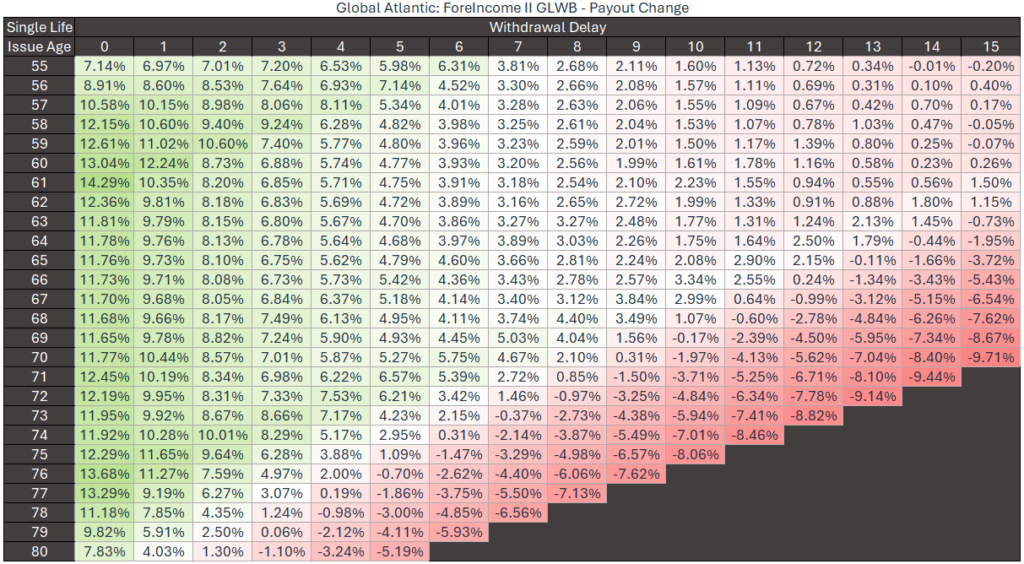

Global Atlantic updated their payout rates for ForeIncome II, while reducing their rollup rate from 12% to 10%. These changes resulted in payout increases at younger income ages and decreases at older income ages. See the table below to see how these adjustments look over all issue age and deferral year combinations.

Global Atlantic last appeared in our snapshot in August 2025 with Income 150+ SE. This rider was relevant in both immediate income and 1-year deferrals, a natural fit given its simple rollup of 7.5% over four years. This is the first time we’ve seen Global Atlantic in our snapshot in the 5-year deferral category. ForeIncome II offers a longer simple rollup of 10% over 15 years, which allows it to compete at longer deferral periods than we’ve seen in the past.

As we previewed last November, Delaware Life with TruePath Income made a substantial change to their payout rates, switching from one-dimensional percentages based on attained age to two-dimensional percentages based on both the issue age and deferral years. This change has little impact on the Ready Growth rider option. But we do see a moderate improvement on the Build Growth rider option, pushing this rider back into third in our age 70 income category.

National Western continues to lead in the 1-year deferral payouts for issue ages 60, 65, and 70, with Income Outlook Plus 5 and its Plus 5 NH variant leading the way, followed closely by the slightly lower Income Outlook and NH variant. These riders are available across a large portion of National Western’s FIA lineup. IMPACT 10 is their top selling GLWB product; currently offering a 7% premium bonus. This means that when paired with Income Outlook Plus 5, the benefit base effectively receives a 12% boost in year one. The Ultra Future product from National Western offers an even richer bonus structure, with a 9% premium bonus leading to a 14% increase in the benefit base in year one — one of the more striking first-year boosts in the current market. We include the Ultra Future product in our snapshot as it currently represents National Western’s highest available payout option.

A few other notable changes from the past month don’t appear in the competitive rankings below. North American increased payout rates for Income Pay Pro across the board by 0.50%. SILAC increased the premium bonus of Denali Bonus 10 Evolve from 17% to 20%. Nassau updated payout rates for Personal Protection Choice. None of these product updates led to substantial changes in payout positions.

For the standings, we look at commissionable FIA products that are sold primarily in the IMO channel. We only include the top products for each carrier that fit this profile. Bolded products either have seen changes to their payouts or are new to the competitive standings compared to the previous month. Below are the Top 3 products and guaranteed income amounts for multiple age ranges and deferral periods:

See you next month. -Caleb Shumpert and Jayden Juergensen

Benchmarks

Fair-Market S&P 500 Caps and Participation Rates

| Date | Option Budget | S&P 500 Cap Rate | S&P Par Rate |

| 3/13/2026 | 5.05% | 9.35% | 54.05% |

| 3/6/2026 | 4.83% | 8.89% | 55.08% |

| 2/27/2026 | 4.78% | 8.94% | 56.54% |

| 2/20/2026 | 4.76% | 8.84% | 55.66% |

| 2/13/2026 | 4.85% | 9.16% | 56.69% |

| 2/6/2026 | 4.88% | 9.28% | 56.98% |

| 1/30/2026 | 4.87% | 9.30% | 59.18% |

| 1/23/2026 | 4.88% | 9.40% | 60.21% |

| 1/16/2026 | 4.83% | 9.23% | 59.47% |

YTD Index Returns as of 3/12:

- S&P 500: -2.03%

- Nasdaq: -2.84%

- Dow Jones: -2.88%

Treasury Yields (week over week change, as of 3/12)

1-year: 3.66% (+7 bps)

2-year: 3.76% (+19 bps)

3-year: 3.75% (+16 bps)

5-year: 3.88% (+16 bps)

10-year: 4.27% (+14 bps)

20-year: 4.86% (+15 bps)

30-year: 4.88% (+14 bps)