MYGIA Madness: The Next Cinderella Story?

The Madness is Upon Us

Each year beginning in late March, 68 division one basketball teams compete in each of the NCAA’s Men’s and Women’s Basketball Championships in what is undoubtedly the greatest single-elimination tournament in the world. Appropriately dubbed March Madness, the tournament has a bit of everything: dramatic upsets, buzzer beaters, heartwarming stories, and a packed slate of games that can keep any casual sports fan glued to the television for hours at a time. Everyone loves to root for an underdog, and there is nothing more thrilling than a true “Cinderella Story” – a previously-unknown team that defies all odds and slips by perennial powerhouses to make it deep into the tournament.

Hold on, Does Basketball Have Anything in Common with the Annuity Market?

Sure it does! Simply consider some of the iconic duos of our time and the answer is obvious:

- Batman and Robin

- Peanut Butter and Jelly

- Mario and Luigi

- Basketball and Annuities

Okay, on second thought, not really. BUT, if really stretching the imagination, one can make the argument that just like there are Cinderella basketball teams in March Madness, there are potential Cinderella products in the annuity market. Take Registered Index-Linked Annuities (RILAs) for example: the niche hybrid product that split the difference between Variable Annuities (VAs) and Fixed Indexed Annuities (FIAs) once had to fight tooth and nail for every sale, being outsold by VAs at magnitude of 80:1. In 2024, RILAs outsold VAs for the first time in the history of the annuity market. Once a Cinderella, RILA is now the belle of the ball.

Today, Multi-Year Guaranteed Annuities (MYGAs) and FIAs are the Blue Bloods of the product landscape and RILAs and VAs are also expected to contend for heaps of sales. Flying under the radar, however, is a product that has all the makings of a true Cinderella Story. It doesn’t have a storied history. Many have never heard of it. But there’s a lot to love about it.

The newest Cinderella Story of the annuity market? The MYGIA.

There’s No “I” in Team… But There is in MYGIA

Google searches and surges in popularity often go hand-in-hand for teams that go on a Cinderella run. Saint Peter’s University and guard Doug Edert’s mustache were all over the internet in 2022 when they made it to the Elite Eight as a 15 seed—just take a look at the graph on Google Trends for the team:

The University of Maryland, Baltimore County saw a leap in undergraduate enrollment on the heels of their historic upset as a 16 seed over 1 seed Virginia in 2018. Prior to their magical runs, if you asked anyone about the basketball programs of either of these schools, a confused face would have been the result. If you have a similarly confused face and are asking yourself “what the heck is a MYGIA?” – you are not alone.

In simplest breaking-down-the-acronym terms, a MYGIA is what many in the industry can probably deduce: a Multi-Year Guaranteed Indexed Annuity. In other words, an annuity with two elements: 1) a component that offers some sort of guarantee over multiple years, typically a rate (fixed, cap, par) or minimum interest credit, and 2) performance that’s linked, in part, to the performance of an underlying index like the S&P 500. Though the two elements of a MYGIA seem straightforward, they can manifest themselves in many ways.

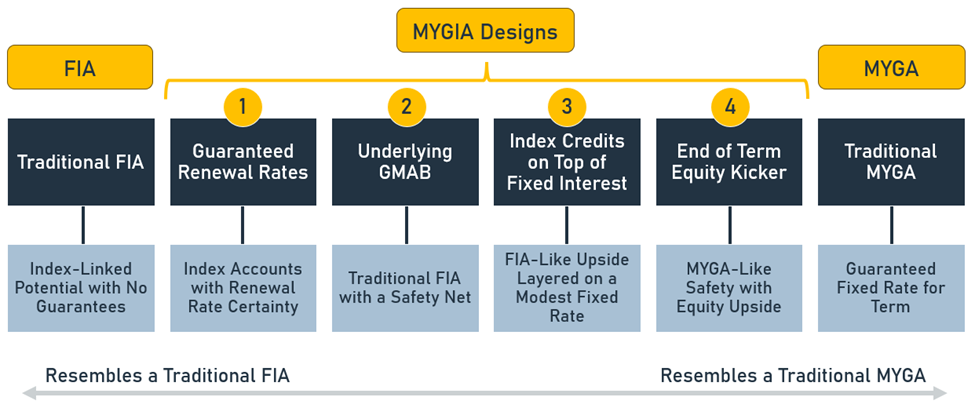

The MYGIA Spectrum

MYGIAs share similarities with both MYGAs and FIAs but are inherently different. Traditional MYGAs are pure fixed rate products with returns that are indifferent to market performance. Traditional FIAs utilize index accounts to link performance to the returns of underlying indices but offer zero accumulation guarantees. In an illustration’s 0% return scenario, a traditional FIA starts and ends at the same Contract Value. The MYGIA “category” is really a catch-all for any product that blurs the lines between traditional MYGAs and FIAs.

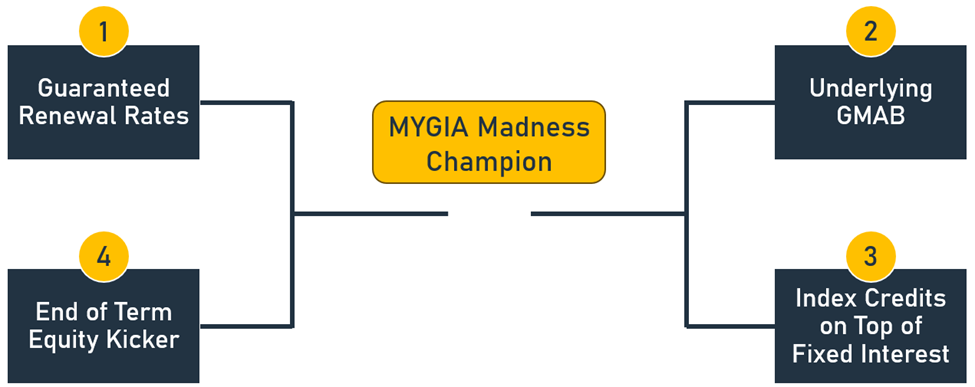

The graphic above splits “MYGIA” into four buckets we’ll dive into in more detail, but the beauty of being in the gray area between FIAs and MYGAs is that there are many variations of these that could all be considered their own type of MYGIA.

MYGIA Design #1: Guaranteed Renewal Rates

Imagine: a FIA that guarantees renewal rates on a 1-Year S&P 500 Cap for the entirety of the withdrawal charge period. Easy to picture, right? This design—one that we would argue is the most to-the-definition version of a MYGIA—is already taking the market by storm. In response to concerns and complaints from clients and producers about renewal rate uncertainty, annuity carriers have taken it upon themselves to guarantee renewal rates on some (or in some cases, all) index accounts within a product to alleviate the all-too-real fear of the notorious “bait and switch” that so many have experienced with a strong initial rate and a quick, steep decline in renewal years. This MYGIA is a Fixed Indexed Annuity, but with multi-year guarantees on the crediting rates: a Multi-Year Guaranteed Indexed Annuity. Apropos, no?

If the shift from annually declared renewal rates on FIAs to ones that are guaranteed for term feels familiar, it’s because it is. It was not too long ago when the fixed rate annuity space went through the same shift. Products with strong first-year rates that were offered to lure in clients were a significant part of the fixed annuity market. The issue, obviously, was what followed – annually renewing rates that had the potential to be significantly lower than the initial rate, even while the product was still subject to withdrawal charges. As more and more people were burned by poor renewals, clients and producers turned to the certainties offered by MYGAs—even if it meant sacrificing some of the first-year rate—in order to secure renewal rate stability.

We are seeing the exact same thing happening to traditional FIAs. Carriers like Global Atlantic, MassMutual Ascend, Pacific Life, Delaware Life, and Securian all offer FIAs with an S&P 500 Cap that is guaranteed for the entire withdrawal charge period. Other carriers, like North American (NAC Guaranteed Allocation) and Pacific Life (Pacific Index Foundation), have launched MYGIAs—keep calling them FIAs if you want—that guarantee rates on all index accounts through the end of the withdrawal charge period.

MYGIA Design #2: Underlying GMAB

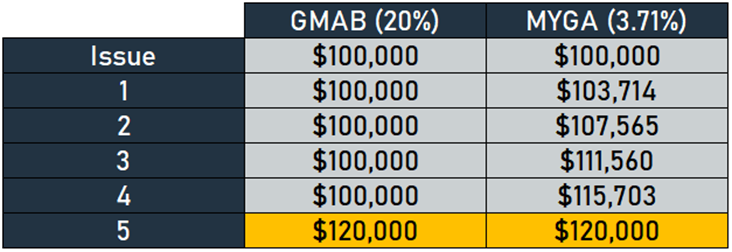

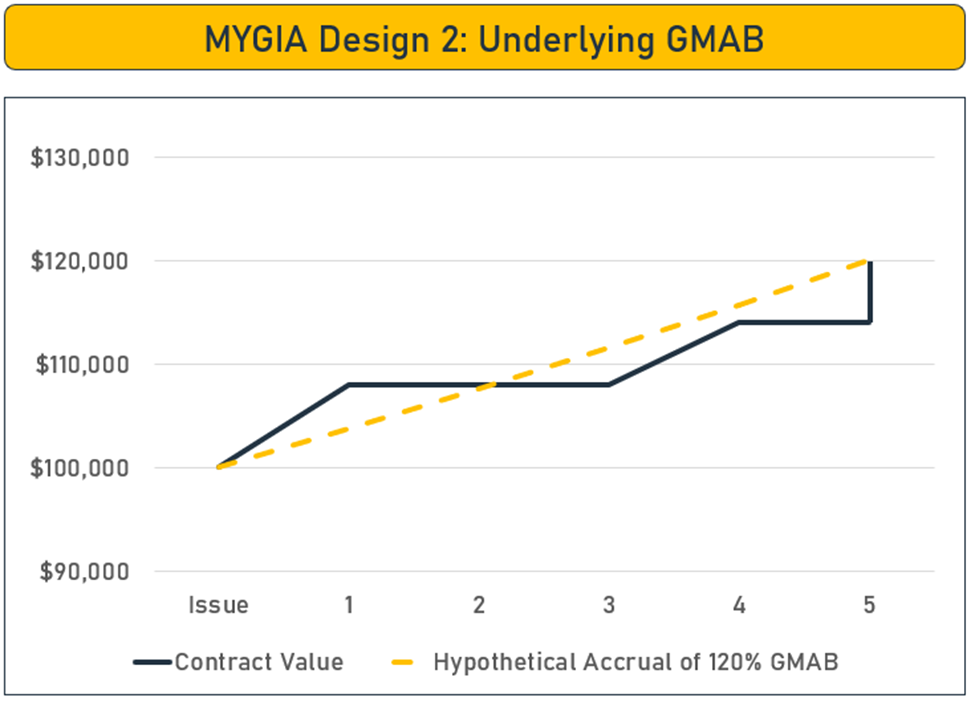

Why decide between a FIA and a MYGA when you can look back and choose the better of the two? In a nutshell, that is what layering on a Guaranteed Minimum Accumulation Benefit (GMAB) to a traditional FIA helps accomplish. Offered originally in the variable annuity space to quell concerns over a significant market drop that could erode accumulated gains and premium, the GMAB in this MYGIA design is intended to give a client a degree of certainty regarding how much interest they will accumulate.

Through the use of a GMAB, this MYGIA design provides an elevated worst-case scenario for the client—essentially, a MYGA-like safety net. Take a 120% GMAB on a 5-year annuity, which promises to deliver at least $120,000 to a client that invests $100,000 at the beginning of the 5-year period. While the GMAB is (or isn’t) triggered all at once at the end of the five years based on the performance of the index accounts, we can think of it as a secondary MYGA account value that is growing behind the scenes at a compounding ~3.71%.

The difference between the GMAB and the hypothetical secondary MYGA account value matters in the years leading up to the potential GMAB payoff. Decrements due to death, surrender, or annuitization prior to the end of the withdrawal charge period do not benefit from the underlying guarantee and therefore could result in a more traditional FIA payoff. Though a minor distinction, that difference provides carriers with a small amount of additional pricing power that can either be directed back into the product or used to increase profitability.

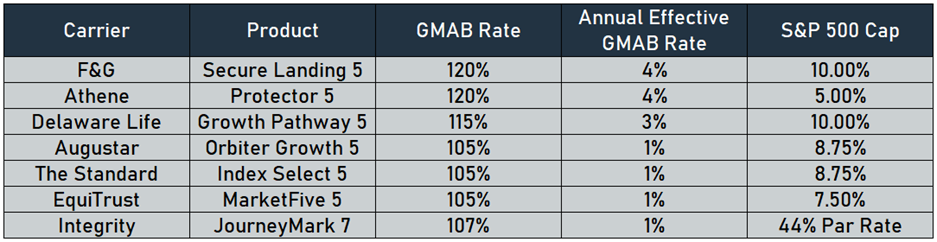

We have seen a fair amount of this design in the industry. Athene, Augustar, Delaware Life, EquiTrust, F&G, Integrity, and The Standard all offer products with some form of minimum interest guarantee feature. Whether explicitly called a GMAB or not—likely by design to avoid distributors classifying them as annuities with a living benefit that typically command higher compensation levels—they are all GMABs.

There is a clear split between the carriers offering a meaningful GMAB benefit and those offering a minor one that, from a pricing perspective, is essentially worthless. Oddly enough, two of the top three companies on the list, F&G and Delaware Life, lead the pack in the S&P Cap offered in conjunction with the guarantee, currently at 10% each.

Athene, the other carrier offering a more meaningful GMAB (albeit with a lower S&P Cap), received approval on a new GMAB that may be intended for use with their more popular products. The Minimum Interest Credit rider included in the filing hints at a 120% GMAB (available with or without a Return of Premium benefit) that aims to broaden the adoption of this strategy with a meaningful guarantee. We expect more to follow with the simple story: index-linked crediting on the upside, guaranteed growth as a backstop.

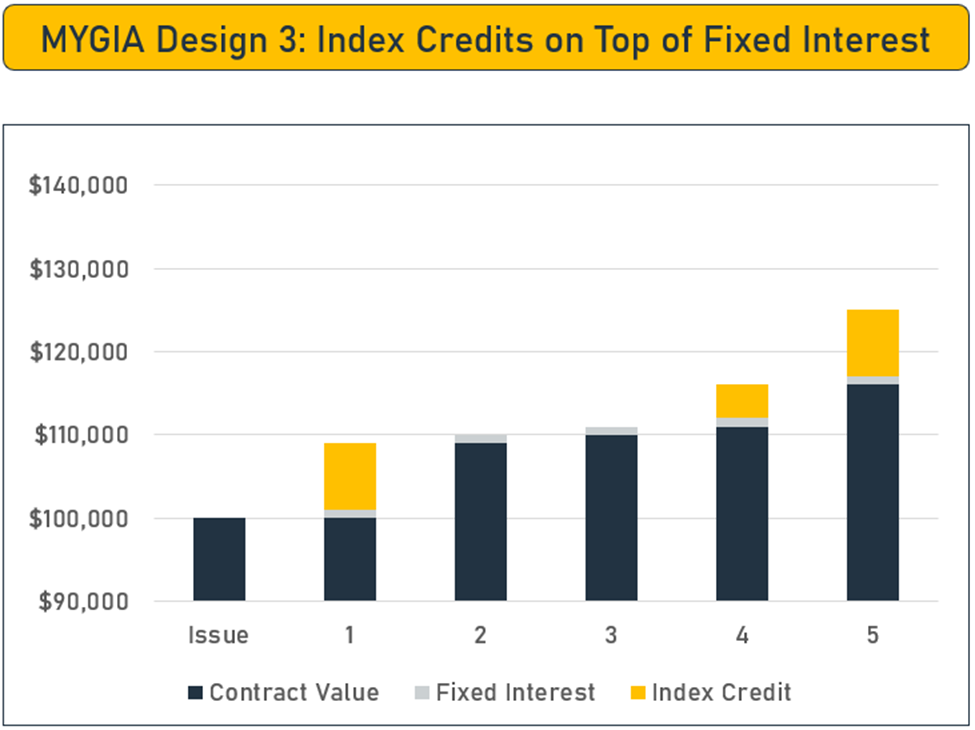

MYGIA Design #3: Index Credits on Top of Fixed Interest

As we continue on the spectrum of MYGIAs toward ones with more of a MYGA flavor, ones that offer annual index-linked credits on top of fixed interest—a “stacked” design—are next on the list. Though not as common as the previous MYGIA designs, the appeal of this design is its best-of-both-worlds hybrid nature. The upside-potential value proposition of a traditional FIA is retained and accompanied by an annual performance floor greater than 0% that is immediately reflected in the Contract Value. Where MYGAs provide fixed rate certainty and traditional FIAs provide a wide range of outcomes, this design aims to narrow the range of outcomes by lifting the floor and limiting the upside.

In discussions focused on “avoiding zeros” in index-linked products, this design should find its home. As trivial as it may seem, a producer being able to explain that the worst-case scenario in a year is low level return, like 1%, rather than a goose egg is a big deal. It comes at a cost, of course. Rather than offering a fair-market S&P 500 cap of roughly 9.50%, a MYGIA that offers a 1% performance floor may only be able to support a cap of 8% with the same budget. Though a wider gap in terms of potential upside, the psychological difference between a guaranteed performance floor of 0% or 1% is arguably a lot more impactful than the 1.50% difference between caps of 8% and 9.50%. We have not seen many examples of this design in the market, but it is out there. American Equity’s BalanceShield offers a positive floor on the index-linked accounts, and as we covered in last week’s Week in Review, The Standard received approval on a “Tiered Index” option which provides a fixed credit regardless of the index performance, plus potential for additional index-linked gains. For clients on the fence between a MYGA and a FIA, this type of MYGIA seems like a slam dunk.

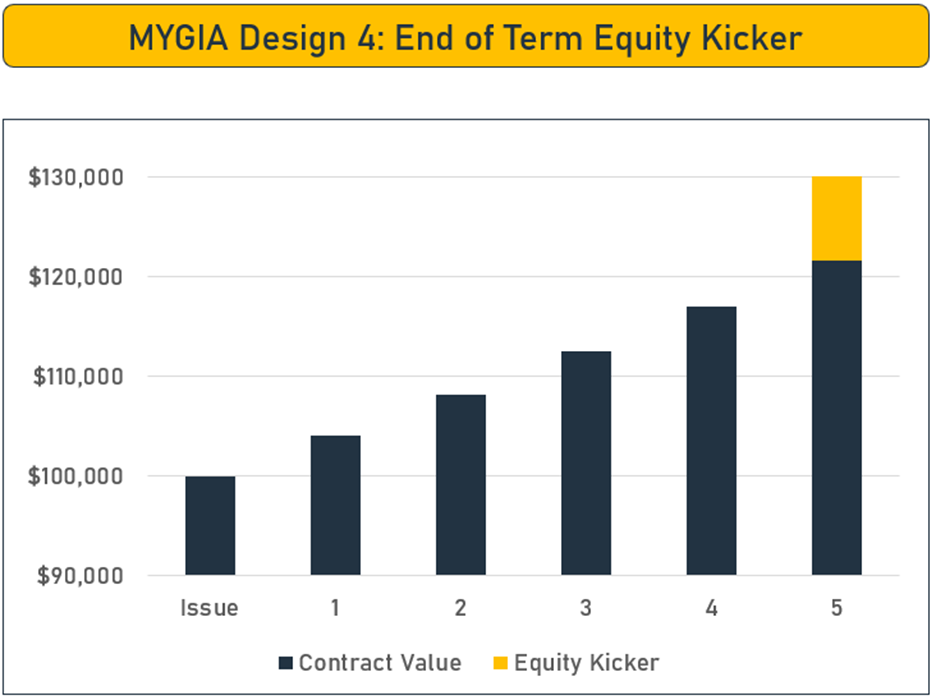

MYGIA Design #4: End of Term Equity Kicker

The final MYGIA design is one that feels among the most likely to find a foothold in the future of the annuity market—akin to everyone’s favorite double-digit seed picked to make it to the Sweet Sixteen. It looks and feels like a MYGA through the withdrawal charge period, offering the stability of guaranteed accumulation at a fixed rate. The “I” in this MYGIA design comes in the form of an index-linked equity kicker at the end withdrawal charge period. This kicker is the type of feature that might be used to sway the opinion of a client torn between the safety of a traditional MYGA and the fear of missing out on upside potential of a FIA.

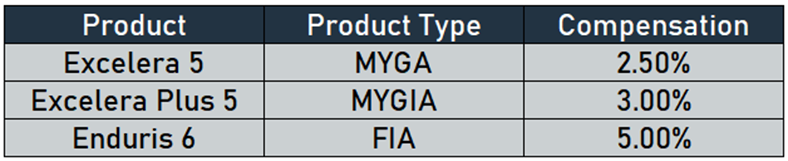

Revol One has blazed the trail of this MYGIA design with their Excelera Plus product. The mirror image of the second MYGIA design that used an underlying GMAB to accompany traditional indexed-linked crediting, Revol One’s Excelera Plus flips the script by crediting a guaranteed rate and providing a one-time opportunity for index-linked upside at the end of the withdrawal charge period. Currently, the five-year version of the product offers a 4% MYGA rate and a 60% participation rate on the S&P 500 that work in tandem. At the end of five years, the client gets the better of the two: the 4% compound growth provided by the MYGA component or 60% of the growth in the S&P 500 over the same period of time. As currently designed, a 60% participation rate would beat a 4% compounding rate with at least a ~36.1% return in the S&P 500 over five years, which roughly equates to a 6.4% annually compounding return—well below the index’s historical average.

Kudos are due to Revol One, which appropriately decided to label the product a MYGIA in their marketing materials due to its hybrid nature. The product hasn’t had much success yet: it came short of achieving even $10M in sales in 2024. It is up for debate if the lack of immediate success is due to the MYGIA design being unique or Revol One being a new entrant to the market—Excelera Plus was one of the first two products launched by the carrier in April of 2024. In all likelihood, it is a combination of the two. The Savings Bank Mutual Life Insurance Company of Massachusetts (SBLI) followed Revol One’s MYGIA with their own Market Crest MYGIA a few months later in August of 2024. The Market Crest design is nearly identical and begs the question: are more copycats on the horizon?

Is the Excelera Plus/Market Crest design the only way to tackle this version of MYGIA? Of course not. Other imaginable variations of this design could include a cap or performance trigger instead of a participation rate. Rather than comparing two accounts, the index-linked performance could be purely additive to the underlying MYGA’s performance. The possibilities are numerous and ripe for innovation.

The Compensation Conundrum

A sticky detail of the MYGIA concept is where producer compensation should land. Typically, producers expect to be paid higher commissions on FIA sales than MYGA sales to compensate them for navigating and articulating the additional layer of complexity that comes with index-linked products. Should index-linked performance, no matter how complex, lead to compensation levels that are more in line with traditional FIAs? Should the guarantees and simplicity of the designs be accompanied by compensation that resembles that of traditional MYGAs? Or, as a blend of the two traditional products, should the compensation on MYGIA fall somewhere in-between? Per Annuity Rate Watch, Revol One, thinks the answer is the latter:

It is not a down-the-middle compensation split for Revol One, and that makes sense: this MYGIA design most closely resembles a traditional MYGA on our MYGIA spectrum. The issue? Paying 2% less on the MYGIA than the FIA is going to steer producers away if they think they can sell their clients on more traditional FIA products.

It is a fair, albeit frustrating, hurdle that MYGIAs that pay less than FIA comp will face. Until MYGIAs firmly find their foothold in the market, producers will compare them against the non-MYGIAs they are considering and notice the stark difference. Though producers are expected to act in the best interests of their clients, any bump in compensation—between products offered by different carriers or between product categories—is an incentive. Though Reg BI was a step in the right direction for the broker-dealer and bank channels in 2020, it only requires that producers “consider reasonable alternatives” under a firm’s Care Obligation. Largely, this has been interpreted to mean considering similar products offered within the same product category, so it may do little to draw attention to MYGIAs.

To remove conflict of interest concerns related to compensation levels, many firms have elected to “levelize” compensation among products offered within the same category, but this has its own issues. Since there are so few in the market today, MYGIAs are unlikely to have their own category at a firm that levelizes compensation. If a firm classifies a MYGIA as a MYGA, it may be less likely to sell due to the additional complexity and salesmanship required. If a firm classifies it as an FIA, the carrier will need to pay FIA-level compensation on it, likely decrease the level of guarantees—and therefore attractiveness—of the product. And if the same product is classified differently by separate firms, carriers will have a difficult time managing the pricing levers of the product.

If producers think they are going to be able to convince their client on some level of index-linked performance, they are going to want to sell a traditional FIA every time. A crude replication of a MYGIA could simply involve allocating a portion of premium to the fixed account within an FIA. Though this strategy allows the producer to capture FIA-level compensation, it may not address a client’s needs as well as a MYGIA that is specifically optimized for that objective.

That is why the key to the success of MYGIAs may begin at the other end of the spectrum. MYGIAs are a great opportunity for producers that typically sell MYGAs (and therefore expect MYGA compensation levels). If designed and marketed appropriately, a MYGIA should be able to retain almost a MYGA-level of simplicity. Positioned to typical MYGA clients, producers could see success pitching the hybrid design and benefit from increased levels of compensation from those that buy into the product. For a producer used to selling MYGAs, MYGIAs could be a great way to dip a toe into the index-linked market without feeling the need to be an expert on everything the industry has to offer.

A Champion of MYGIA Madness?

Unlike its basketball counterpart, more than one champion can emerge from MYGIA Madness. These designs, in their totality, fill a hole in the annuity market. We have already seen carriers blurring the lines between FIAs and MYGAs, but MYGIAs have a long way to go—in terms of both compelling products and overall category sales—to play serious ball with the Blue Bloods. If more and more carriers push into the MYGIA spectrum from one end or the other, the market will respond. Rate aggregators will create MYGIA categories, producers will learn to sell them, and more clients will be served by products that best meet their needs.

Though mostly unheralded underdogs today, MYGIA products—ones launched, and ones being developed—have all the makings of a classic Cinderella: plenty of doubters, a story to be told, and reasons to believe. -Jon Blomquist