S&P 500 Cap Rates in FIAs

Are the cap rates that life insurers offer of FIAs too high right now? At Life Innovators, we’ve kept track of the fair market cap rates for S&P 500 strategies since June of 2022. There’s one thing we’ve continually noticed; there are always a handful of life insurers that are head and shoulders above the rates we would expect. So, why does our benchmark not match what we see play out in the market for a subset of life insurers?

Let’s dig into what we think some carriers are doing, and what it could mean for an end consumer.

FIA Rate Comparison

First, let’s look at our current fair market cap rate on the S&P 500. These rates are what we deem fair for a market-consistent 10-year FIA given the current economic environment.

| Option Budget | S&P 500 Cap Rate | S&P Par Rate | |

| 6/21/2024 | 4.80% | 9.16% | 60.86% |

| 6/14/2024 | 4.84% | 9.33% | 62.11% |

| 6/7/2024 | 4.82% | 9.18% | 61.16% |

| 5/30/2024 | 4.99% | 9.42% | 62.26% |

| 5/23/2024 | 4.89% | 9.25% | 61.52% |

| 5/8/2024 | 4.92% | 9.59% | 60.94% |

| 5/1/2024 | 5.08% | 9.77% | 60.21% |

As of 6/21, the current fair market cap is 9.16%.

Now, let’s look at current rate offerings in the FIA marketplace. If we look at 10-year FIAs, and products that do not have a fee or buy-up on the S&P…

There are currently 20 products in-market in the IMO channel with cap rates that are at least 2.00% higher than the fair market rate of 9.16% (in other words, cap rates ≥ 11.25%).

How’s that possible?

It’s important to first look at how we calculate our fair market cap rate.

To do so, we use a Black-Scholes pricing model with the following inputs:

- Risk Free Rate: 12-month CME Term SOFR

- S&P 500 Dividend Yield

- Moody’s Baa Seasoned Corporate Bond Yield

- Volatility: 12-month SPX implied volatility using 3rd party institutional data

- Assumed Pricing Spread of 1%

At a high-level, Moody’s Baa Yield is a proxy for carrier general account yields — this is what a carrier can count on coming in each year to spend on options from the asset/liability matched securities they purchase. Then, we assume the carrier will take a spread of 1%. This spread accounts for things like acquisition expenses, carrier overhead, and the required profit margin or cost of capital. The other factors listed help us evaluate the current options market and associated pricing. Simply put, our fair market cap rate is based purely on current market conditions and a down-the-middle investment strategy into institutional fixed income securities.

If you were to think of our FIA rate model as a distance runner who’s running a marathon — we are starting out and finishing the run at the same pace — one that can be maintained for the entire duration of the race. If a life insurer’s offered cap rate deviates significantly higher from what we model, are they privy to some secret sauce that other carriers aren’t? Doubtful. We believe it’s likely they’re doing one (or more) of these things:

- Investing in higher yielding securities

- Making option pricing assumptions

- Subsidizing rates across index options

- Having ultra-competitive rates to gain sales traction

Let’s take a closer look at each of these items individually.

Investing in Higher Yielding Securities

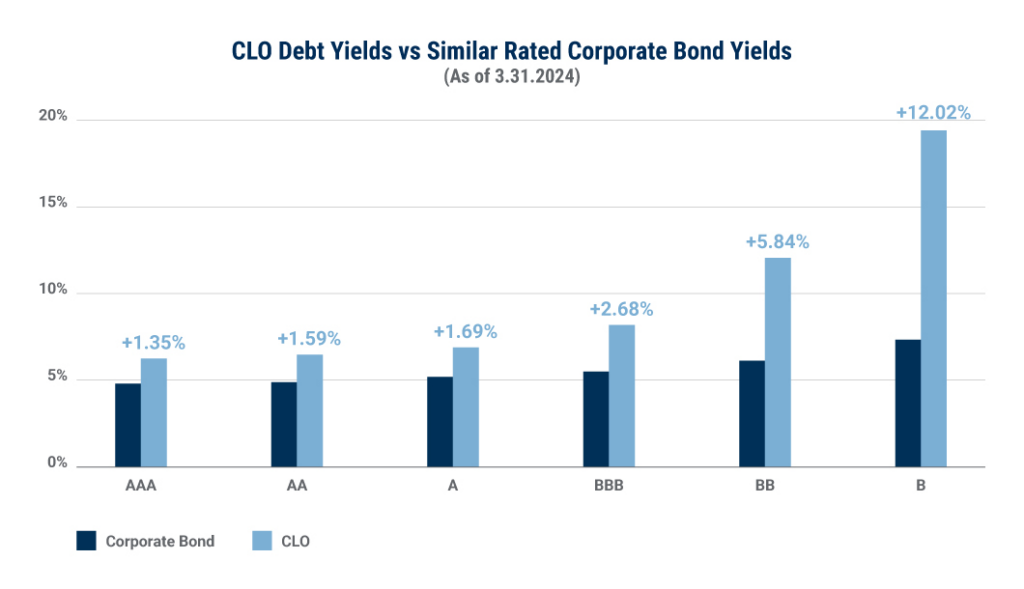

It’s possible life insurers are investing in securities that offer a higher yield than Moody’s Baa Seasoned Corporate Bond Yield. More yield means bigger option budgets, which translates to higher offered rates. Some life insurers have been transparent about their ability to source deals (with higher yield potential) via their strategic asset management partnerships. Other carriers have invested more heavily into collateralized loan obligations (CLOs) and other structured credit securities. These instruments are more complex and less liquid than traditional bonds, but they’re also more diversified and protected from loss because of a residual equity position that takes first loss. As a result, structured credit can deliver higher yields than bonds with the same ratings. See the graph below from Bluerock:

Structured credit and other asset classes such as rated feeder funds are capturing the attention of regulators concerned that life insurers are inadequately capitalizing those asset classes. On one side of the debate are insurers who rightly point out that CLOs and other structured credit instruments have had extremely low historical default rates. On the other side are insurers who point out that the current crop of CLOs and structured credit have benefited from historically low interest rates and may prove to have much higher default rates. In other words, they’re arguing that there is no such thing as a free lunch and the yields of these securities are higher because the risk is higher – regardless of the formal rating.

Where the NAIC lands on this topic will have real impact for insurers who are heavy users of structured credit. If an insurer is pursuing the strategy of this type of asset class, it’s possible that their future capital requirements will increase if the NAIC assigns higher RBC factors. An increase in required capital in the future will either lead to lower returns to the carrier or will be passed through to the customer in the form of lower renewal rates.

To go back to our racing analogy, if this were another runner in the same marathon, this would be someone who starts out with a much faster pace at the beginning. They establish themselves at the front of the pack, while hoping they have the wind to maintain their lead — but there’s a possibility they gas out before the finish line.

Making Option Pricing Assumptions

Another potential method for high cap rate offerings is to make assumptions about the future price of options. Instead of using current option prices, carriers might assume that if interest rates go down in the future, the price of future options will also decrease, thus increasing their profitability. With interest rates being high right now, relatively speaking, lower interest rates will cause future option prices to decrease. In essence, there’s a smoothing that’s happening. Life insurers are giving up some level of profitability early on, assuming option prices will decrease in future years and ultimately hitting their rate of return targets by the end the product term, all white holding rates steady.

This runner starts the race strong, and they’re banking on the course getting easier and more downhill later into the race, which allows them to cruise more easily into the finish line. If it doesn’t and it’s more uphill (if interest rates increase or volatility spikes in the future) option costs could go up. This would force a carrier to either stomach the loss or lower their renewal rates to maintain their profitability targets.

Subsidization Across Index Options

Contrary to popular belief, not all index options are created equal inside of FIAs. A life insurer might have an extremely competitive S&P 500 cap rate alongside other engineered (volatility-controlled) indices with participation rates and/or a Fixed account. A carrier is not obligated to spend their entire option budget on each individual index. They can pick and choose how they want to internally price each index. Let’s look at an example.

We’ll assume Life Insurer A has a 5% option budget.

The S&P 500 strategy they currently offer with a 12% cap rate costs 5.5%.

The engineered index they offer has an option strategy that costs 4.5%.

The carrier assumes 50% of index allocations will go into the S&P 500, and 50% will go into the engineered index. By making this assumption, and if it pans out, the total cost to the life insurer will be 5%, or exactly what they have available in their options budget.

With our same analogy, this runner has some teammates on out on the race course with them. They hope they can use their other teammates to draft behind, and slow down their headwinds, ultimately running a quicker race than they could on their own. However, what if those teammates are nowhere to be found once out on the race course (too much money flows into the S&P 500 strategy)? This would effectively cost the life insurer more because they’re spending more for the S&P option than they planned, ultimately driving down their profitability.

Again, life insurers can eat this cost, or lower future renewals on their index offerings.

Having ultra-competitive rates to gain sales traction

For new carrier entrants, gaining FIA market share is no easy feat. They need a competitive advantage — something to give producers a reason to get contracted and do business with them. There’s a handful of levers that can be pulled to achieve this, with one of those being pure rate. In other words, have one of the highest S&P 500 cap rates available in the marketplace. To round out our analogy, this is as if the runner is in a marathon but has decided to win the first segment rather than the race. And as any runner knows, if you start fast, you’re going to end slow – usually very slow.

Conclusion

At Life Innovators, we try to price our current benchmark cap rates fairly based on current economics. If a carrier’s offering a cap that’s significantly higher than our fair market rate, there’s some level of assumption dependency going on at the carrier level. Those assumptions may or may not pan out. If all goes well, clients will see the benefit in the form of high, sustained cap rates for the entire term of the product. If not, it could lead to lower future renewal rates, which doesn’t bode well for clients or producers. -Sam Wiss