The Slippery Slope of Subsidization

There’s a number by which every FIA is judged: the S&P 500 cap. It’s the figure that dominates sales presentations, drives competitive positioning, and often determines whether a product flies off the shelf or collects dust. But here’s what most people don’t realize. That shiny, competitive cap plastered across marketing materials might actually be a modest crediting budget wearing a very expensive disguise.

The FIA industry has developed an open secret when it comes to supporting a competitive product. To compete in a crowded market, many carriers artificially inflate their headline S&P 500 caps by quietly suppressing rates on other indexed accounts and/or borrowing pricing power from future renewal years. Welcome to the world of rate subsidization. It’s a world where renewal rates might drop not because markets moved, but because too many other consumers chose the “wrong” allocation. This isn’t a story about a few bad actors, it’s about an industry-wide practice that has become so normalized that carriers who don’t play the game risk irrelevance.

FIA Rate Setting 101

Let’s start with a crash course on annuity rate setting. The insurer collects premium from consumers and uses it to purchase various assets, such as corporate bonds and mortgages. The rate setting process starts with an estimate of the yield the insurer can earn on those assets. Using actuarial pricing models, the insurer determines in advance what portion of that yield needs to be kept to cover its expenses, reserve for expected benefit payments, and earn their target profit margin. The remainder of the yield becomes the “crediting budget”, representing how much the insurer can spend on crediting interest to its contracts. For a fixed annuity such as a MYGA, this amount is a target for the crediting rate itself. For an FIA, interest isn’t credited via a clear-cut fixed crediting rate, but rather through index caps and participation rates. In that context, the crediting budget represents how much the insurer can spend to purchase derivatives that replicate the payoffs of the FIA crediting strategies. From there, the insurer essentially backs into the cap or participation rate whose replicating derivative portfolio has a cost equal to the crediting budget.

Most FIAs offer multiple indexed account options, whether it be different indices, different crediting methods, or different crediting terms, and this adds another wrinkle to the carrier’s rate setting decisions. The crediting budget we described above represents the total the carrier can spend on a block of new business. But how does that get apportioned out to each indexed account? One approach is to divide it up evenly—that is, target the same crediting budget for every indexed account. Another approach is to spend more on some options and less on others, such that the weighted average across options aligns with the aggregate crediting budget. This idea is precisely what we mean by “subsidization”. What does this look like in practice? Let’s walk through an example.

Meet Aspiring Life

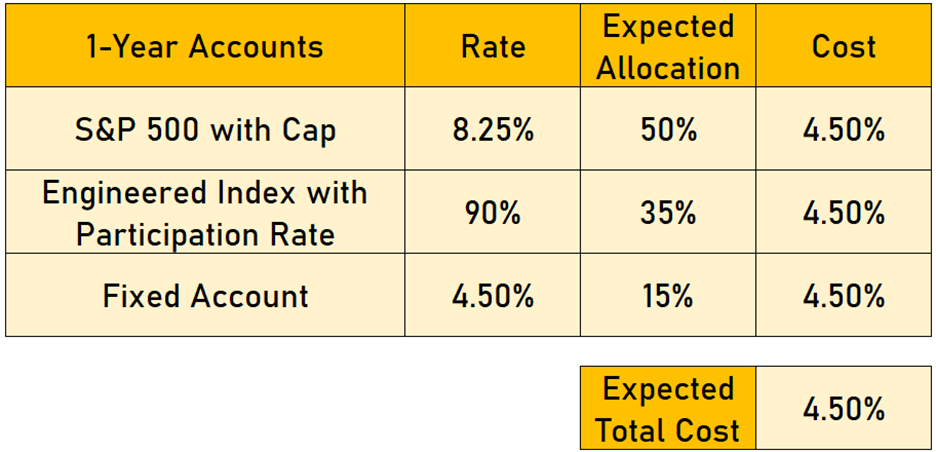

Consider the hypothetical insurer Aspiring Life. The company has traditionally sold fixed annuities, but has been watching the FIA market and is attracted to the growth opportunities it presents. Aspiring Life is gearing up to launch their first FIA, which will be positioned in the market as accumulation-focused product without any premium bonus, income rider, or enhanced death benefit. In line with all that we have outlined above, after accounting for their investment strategy, expenses, reserve requirements, and profit margin, Aspiring Life’s pricing model indicates a crediting budget of 4.50%—which they’ve been told is a reasonable crediting budget in today’s environment. As a new entrant, Aspiring Life has decided to lean toward a simple account lineup, made up of just two indexed accounts and a fixed account.

Strategy A: No Subsidization

Aspiring Life begins working through their rate setting strategy in preparation for their upcoming launch. To keep things simple and straightforward, Aspiring Life determines target crediting rates for each of their three accounts based on the same 4.50% crediting budget. By spending the same amount on each of their three accounts, Aspiring Life would expect to pay 4.50% to support the rates on the product no matter where their customers allocate their premium—an appealing result for a new entrant with no live experience to use to make a confident allocation assumption.

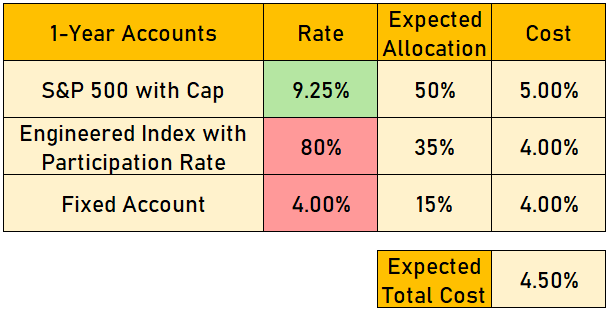

The problem is that their top competitor, Aggressive Life, offers an S&P 500 cap of 10.00%. At 8.25%, Aspiring Life’s product would probably not be able to compete with Aggressive Life, despite a relatively strong crediting budget. Aspiring Life is already being about as aggressive as they can be to get to a 4.50% crediting budget, so they can’t just magically find more yield. Rather than roll over and admit defeat, what can Aspiring Life do to put together a more compelling product?

Strategy B: Subsidize a Strong S&P 500 Cap

Just like a host of fellow insurers in the space, Aspiring Life can make the decision to increase the S&P 500 cap account and decrease their other accounts to make up for it. Fair or not, sales in the accumulation-focused FIA space are driven mainly by the competitiveness of a carrier’s S&P 500 cap. Rates on engineered indices are not as heavily commoditized, due in part to the diversity of index options in the industry and inability to compare apples to apples. If the company’s assumed sales mix is right, they can expect to see the same aggregate cost emerge from the product. Aspiring Life decides not to go so far as to push themselves to the very top of the S&P 500 cap leaderboard for their initial launch, but with a little bit of subsidization magic, they are still able to significantly shrink the gap between the 8.25% cap that their initial pricing suggested and the 10.00% cap offered by Aggressive Life.

What If Allocation Assumptions Go Wrong?

Subsidizing the S&P 500 cap as demonstrated above certainly could work out well for Aspiring Life, but it is far from certainty. As any pricing actuary can tell you, setting rates can be a bit of a juggling act. When an insurer’s rate setting strategy involves drastically different crediting budget for each account, things can get tricky. A few of the many questions that must be considered while setting rates:

- How has the cost of our current rates been impacted by market movements since our last rate change? How does that compare to our crediting budgets?

- How will the proposed rate change stack up against the rates offered by competitors—and will competitors change their rates too?

- Is the proposed rate change making one account more attractive than another?

- What sort of premium allocation has each account been getting? Is there reason to believe that those allocations will begin to shift?

- How will all of these moving parts come together and affect the aggregate cost of offering this product?

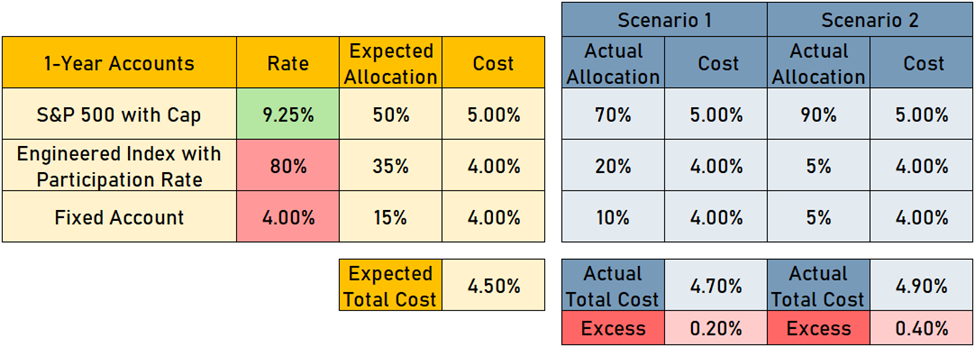

By pushing more of their pricing power into a competitive S&P 500 cap, Aspiring Life could very well see more premium deposited into that account than originally expected. If that happens, the financial ramifications could push their otherwise profitable FIA underwater. Below, consider two hypothetical scenarios where increased allocations to the more competitive S&P 500 cap lead to additional spending on the underlying options used to hedge that account.

In both scenarios, the total cost to support the accounts within the FIA meaningfully exceeds the crediting budget that was available to Aspiring Life. Although the basis points may seem small in isolation, this sort of experience over a large block of business can quickly morph into a significant dollar amount.

Impact on Renewal Rates

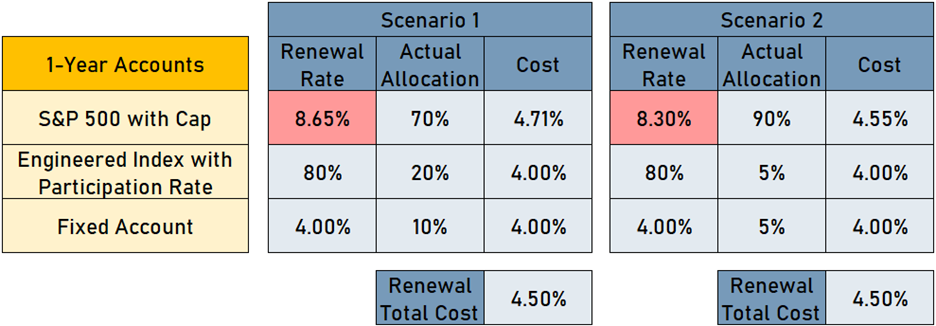

When allocations to a subsidized S&P 500 cap come in higher than expected, an insurer essentially has two options: continue to accept lower profitability or decrease renewal rates to restore margins. Unfortunately for consumers, the latter is often at least part of the answer. By reducing the S&P 500 cap in renewal years, an insurer can get the total cost back in line with their original target. If either of the scenarios above happen to Aspiring Life, their pricing may lead them to make substantial decreases upon renewal.

It’s a simple algebra exercise, but it’s one that has far broader implications than a spreadsheet calculation. How does a producer go to their client after one year of a multi-year FIA contract and deliver the bad news that their S&P 500 cap had to drop nearly a full percent? The producer does not have transparency into the insurer’s account allocations, so their justification may have nothing to do with the actual cause of the drop. If the market as a whole hasn’t moved much and S&P 500 caps on new products resemble the levels they were at when the contract was issued, the producer might be met—justifiably—with a healthy amount of frustration.

Borrowing from the Future

Fast forward a year. Aspiring Life’s FIA business isn’t off to a great start. Thankfully, their first-year allocation assumptions held, but their sales have been ramping up much slower than expected. As is often the case, feedback from distribution partners points to their S&P 500 cap. Despite their best efforts to close the cap gap, it seems that account subsidization has not been enough to pull producers away from Aggressive Life. In hopes of righting the ship, Aspiring Life has hired an ambitious new head of product who promises to have an idea that will solve the fledgling carrier’s competitive challenges.

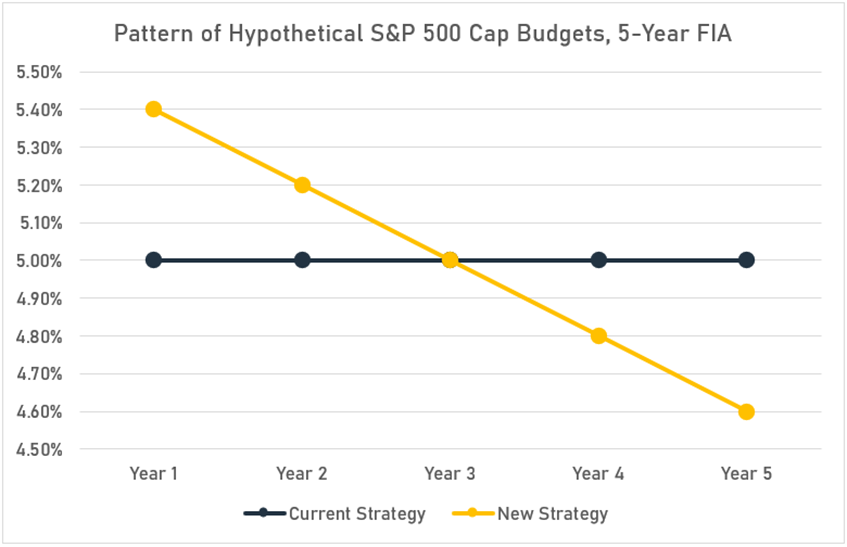

The new hire points out that subsidization is not limited to the way insurers allocate their crediting budget among each account. To improve competitiveness for those seeking the strongest S&P 500 cap, insurers may also subsidize their initial rates by borrowing from their future crediting budget—the budget available to support renewal rates. This subsidization is rooted in the idea that producers and consumers are tolerant of minor reductions in renewal rates. A minor drop here and there can be blamed on “the market” without causing too much concern. The head of product presents the graph below to illustrate a new proposed pricing strategy for Aspiring Life’s 5-year FIA.

The current strategy is to target a constant 5.00% crediting budget for the S&P 500 cap in all contract years. Assuming the investments backing the product are earning a fixed yield throughout the five-year period and allocation experience matches expectations, this strategy is a reasonable one. Over the course of the five years, option pricing dynamics (volatility, volatility skew, dividend yield, risk free rates) may cause the initial cap offered to move up or down in renewal years, but the value of that cap would stay the same.

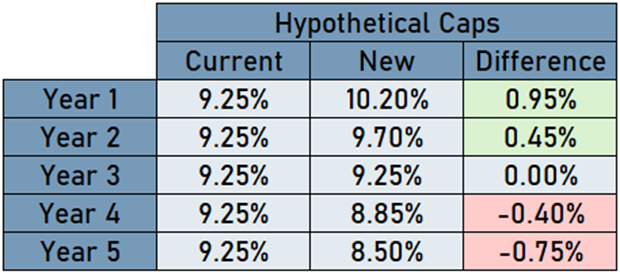

The new proposal, on the other hand, leans into the assumption that minor year-over-year reductions in the cap will be tolerated. Over the five-year period, the average assumed crediting budget is nearly the same as under the current strategy, but under the new strategy, Aspiring Life employs planned renewal rate decreases to subsidize the initial cap. The decline is subtle, resulting in yearly cap reductions of no more than 0.50% if the option pricing dynamics hold. But over the course of the five-year period, the renewal caps would drop by over 1.50%, down well below the 5th-year S&P 500 cap that would be supported by the current strategy. Here’s how those hypothetical S&P 500 caps shake out, assuming stable option pricing dynamics throughout the five-year projection:

Without the clarity of what renewal rates will look like, producers and consumers are left looking at only the first row of the table above, which clearly makes the new strategy look more attractive. A 10.20% cap may seem much stronger, but ultimately both strategies are supported by the same aggregate crediting budget. The new strategy’s borrow-from-the-future approach will now be better able to compete with Aggressive Life’s 10.00% cap. That competitiveness comes at a cost: assuming option pricing dynamics hold, future renewal rates are going to drop. The “market” may still be blamed, but when the real reason for these drops is the strategy set forth by the insurer, the market should not be the scapegoat.

A Double Whammy

What happens when Aspiring Life sets out with the intent to grade down their crediting budget each year, as the new head of product has proposed, AND experiences higher allocations to their ultra-competitive S&P 500 cap than they originally expected? The detrimental duo of planned and unplanned reductions in the crediting budget can cause renewal rates to plummet.

For producers and their clients, it is the ultimate bait and switch. Aggressive allocation assumptions and front-loaded crediting budget patterns are the spark and gasoline that can set trust in the insurer ablaze. This could eliminate any chance Aspiring Life had at establishing a solid reputation in a new market.

Subsidization in Action

Aspiring Life may not actually exist, but there are numerous examples of real carriers facing the same challenges and arriving at the same solutions. To win business in a highly competitive market, many are finding themselves needing to utilize some sort of subsidization strategy in order to boost their headline rate without just giving away the shop.

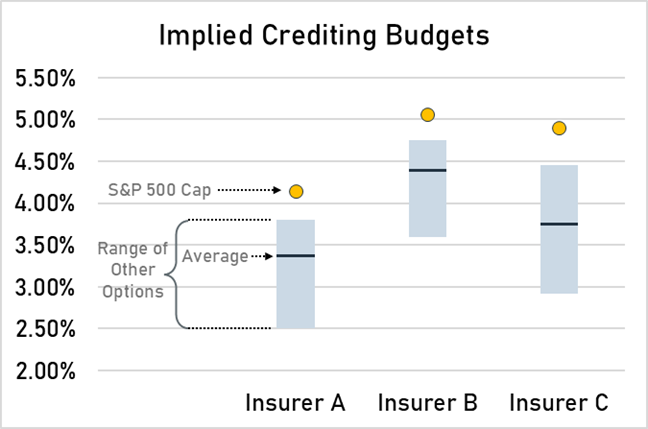

These dynamics aren’t limited to new entrants trying to make a name for themselves—even established carriers that routinely live at the top of the sales charts are playing the subsidization game. We picked three carriers out of 2025’s top 10 FIA writers and calculated the implied crediting budgets of the accounts on their rate sheets. Take a look at the trend that emerged:

All three insurers are spending more on their S&P 500 cap than all the other options we priced. Within this sample, the S&P 500 cap costs were between 30 and 200 bps more than the other options, with an average difference of roughly 90 bps. This is almost exactly the same as our illustrative example for Aspiring Life, and is a strikingly consistent result that demonstrates how prevalent this strategy has become.

Historical Transparency (or Lack Thereof)

Another concerning trend in the FIA industry? How difficult it is to track down information on how insurers have handled renewal rates on their inforce business. Surprisingly, there are no regulatory requirements for an insurer to publish even their current renewal rates, let alone a full history, and as a result many do not. Transparently sharing renewal rate history is not a data issue—the rates are necessarily stored within an insurer’s policy administration system to properly map out how a contract has earned interest over time. Establishing some sort of historical renewal rate repository certainly requires some configuration, but there have undoubtedly been other projects that insurers have invested resources in that have been more complicated and time-consuming but have provided far less value. Unfortunately, a lot of insurers’ lack of transparency likely comes down to avoiding the risk of exposing themselves as a player in the subsidization game.

Thankfully, there are some carriers that are demonstrating the type of transparency that should be commonplace. Nationwide and Pacific Life put out full-blown tables of their entire renewal rate history for all historical issue dates. Lincoln offers a public tool that allows users to select a product, account, and issue date and see a graph of historical rates for that segment. Others like American Equity, Nassau, Securian, and EquiTrust have put together flyers that include statistics speaking to their renewal rate integrity.

Do all of these companies have stellar track records? Not exactly. Some of them look an awful lot like Aspiring Life’s declining line from earlier. But kudos to them for at least being transparent. A view into a carrier’s rate setting history gives prospective buyers an idea of what kind of renewal rate experience they might expect from that carrier. Armed with that information, they can decide for themselves whether they’d be comfortable with a similar experience. Without that transparency, a consumer is left with no idea of what kind of ride they’re in for.

Renewal Rate Certainty

One trend that has emerged to combat renewal rate risk is the concept of guaranteed renewal rates. A growing list of carriers now offer options that function just like a traditional annual point-to-point, but instead of requiring the consumer’s blind trust in renewal years, they include an explicit guarantee that each renewal rate during the surrender charge period will be equal to the initial rate at issue.

For the insurer, this comes with a risk that the cost of hedging each annual point-to-point option will increase in the future and they can’t adjust renewal rates in response. Most carriers find it cost-prohibitive to explicitly hedge this risk, and instead they take an additional margin to cover it. For example, S&P 500 caps with multi-year guarantees tend to be 1-2% lower than the same option with a traditional non-guaranteed structure. The tradeoff for the consumer is this: a higher rate for the first year with no real guarantee of what will happen after that, vs. a lower rate that will stay exactly the same for the entire term.

If you’re a consumer, this seems like a great solution. Let the insurer bear the risk of future market fluctuations, not you. The question is how much that trade is worth—and the answer is, probably not as much as the rates would indicate. For one, multi-year guarantees come with reserve strain for the insurer. In a nutshell, the required asset balance the insurer needs to hold to support the block of business is higher for products with longer-duration guarantees. The insurer’s margin for guaranteed rate options must account for this reserve strain in addition to the “true” risk of the guarantee.

While a guaranteed renewal rate option takes renewal rate risk out of the equation for the consumer, it doesn’t solve the insurer’s allocation risk dilemma. In fact, it exacerbates it. If the insurer spends too much on the guaranteed rate option and gets too much allocation to it, they can’t reduce renewal rates to rightsize their hedge costs in later years. They are effectively haunted by their incorrect allocation assumptions for multiple years. This risk is likely also baked into the rate differential between guaranteed and non-guaranteed options. So while the consumer doesn’t directly bear the insurer’s allocation risk through year-by-year renewal rate decreases, they bear it by accepting a significantly lower-than-fair-market cap and leaving money on the table.

Model Portfolios

Another approach that has emerged in recent years is the concept of the “model portfolio”, which is a collection of preset allocations to specific accounts within an FIA product. Rather than manually selecting individual accounts, an applicant simply elects the model portfolio. Their premium is automatically divided among the constituent accounts and rebalanced to the same percentages on each contract anniversary thereafter. This feature can offer numerous benefits to both the consumer and the carrier.

The obvious benefit to the consumer is convenience—a way of diversifying their FIA portfolio without spending time deliberating about exactly how much they should allocate to each of the available accounts. But the power of model portfolios runs much deeper. By eliminating uncertainty around their allocation experience, carriers employing any sort of subsidization strategy can significantly de-risk their product. The carrier can then redeploy this “juice” into other features that ultimately benefit the consumer as well.

Perhaps the most logical strategy for the carrier is to redeploy this pricing power into subsidization itself. For example, North American’s Guaranteed Allocation product features four model portfolio options, each with a different allocation to the S&P 500 cap account. “Model Blend A” boasts a 12.00% cap on the S&P 500, but restricts this allocation to 20%. On the other end of the spectrum, “Model Blend D” allocates 50% of the premium to the S&P 500, but with a cap of just 7.50%. In essence, North American is doing what almost all competitive carriers do, but in a way that is more transparent and arguably more equitable. Without model portfolios, a contract with 100% of its premium allocated to an engineered index with a less valuable rate is unknowingly bearing the cost of another contract with 100% of its premium allocated to a subsidized S&P 500 cap. By using model portfolios, the carrier can isolate the subsidization such that it only affects those electing the model. That way, the ones who want to chase the highest S&P 500 cap pay for their own subsidization by being forced to allocated a portion to less valuable accounts.

Other carriers have developed their own unique ways of incentivizing the consumer to accept allocation restrictions. Augustar’s OrionShield 10 features a five-tier premium bonus depending on how much is allocated to the S&P 500: if no premium is allocated to the S&P 500, the premium bonus is a whopping 21%; if more than 75% is allocated to the S&P 500, the premium bonus shrinks to just 10%. Talcott’s Everguard Aspire features guaranteed renewal rates, but only if the “Balanced Rate Guarantee” model portfolio is elected, which does not include the S&P 500 at all. This is an example of a solution to both sides of the risks we’ve been describing in this article—an agreement between the carrier and the consumer to solve each other’s problems. It’s as if Talcott is saying, “we’ll give you renewal rate certainty if you give us allocation certainty.”

The Path Forward

The subsidization strategies we’ve explored aren’t inherently evil—they’re rational responses to a market that judges products primarily by a single metric. But when carriers chase headline rates through aggressive subsidization, they create a house of cards that could eventually collapse on consumers through disappointing renewal rates and cross-subsidization inequities.

The good news is that the industry is evolving. Model portfolios, guaranteed renewal rates, and allocation-based bonuses represent meaningful attempts to align carrier and consumer interests. These innovations suggest a path forward where transparency replaces opacity, and where the true cost of competitive rates is borne by those who benefit from them rather than spread across an unwitting pool.

For producers and consumers, the lesson is clear: that eye-popping S&P 500 cap might come with hidden costs. Ask about renewal rate history, understand allocation restrictions, and consider whether guaranteed (but lower) rates might better serve long-term goals than subsidized (but unsustainable) headline rates. In the end, the most competitive rate isn’t always the highest one—it’s the one you can actually count on.

-Drew Schmalz and Jon Blomquist