Week in Review – 8/29/2025

Product Updates

Securian Takes a Ride on the RILA-Coaster

This week, St. Paul, Minnesota’s Securian Financial went live with AccumuLink Advance, their first entry in the RILA category. This product has been a long time coming – we first covered the filing just over a year ago as Securian became the first carrier to take advantage of recent regulatory relief and gain approval of a RILA through the Interstate Compact. By our count, they now become the 23rd carrier with a RILA available for sale. With YTD industry RILA sales at around $35B – a 20% increase relative to the first half of 2024, per LIMRA – Securian is betting that the 23rd seat is still worth the price of entry.

As a later entrant to the space, Securian had the tricky task of figuring out how to stand out in the crowd while still coloring inside the lines the market has established. AccumuLink Advance seems to strike just the right balance. Many of its features are market-standard, which will help Securian wholesalers cut to the chase when introducing it to advisors who are familiar with other RILAs. But there are also a few unique elements in the design that could turn some heads.

In addition to the bellwether indices S&P 500, Nasdaq-100, and MSCI EAFE, the index lineup includes the Janus Henderson Equity Directionality Excess Return Index (JEDI), which is unique to AccumuLink Advance. Built on the concept of buying low and selling high, it looks at 1-day and 5-day returns of the S&P 500 and dynamically adjusts exposure between 50% and 200% depending on the combined directionality. In contrast to vol-controlled indices, this mechanism ends up magnifying the volatility of the index relative to the S&P 500, which makes it well-suited for buffer strategies that tend to thrive on higher volatility. Due in part to the excess return nature of the index, Securian offers 10-20% higher par rates on JEDI than on the S&P 500, depending on the buffer level and crediting period. Performance-wise, the force has been strong with this one – since its inception date of 6/1/2018, JEDI has posted an impressive 14.8% live CAGR, which is 3.6% higher than the S&P 500 over the same timeframe. Higher par rates, higher returns over a 7+ year period of actual live performance, and a catchy name to boot? Hard to argue with that combination.

Another feature that sets Securian’s product apart is the inclusion of a 1% buffer option on all of its indices. This option allows more aggressive buyers to maximize their upside potential if they’re comfortable shouldering almost all of the downside risk. Compared to the corresponding 10% buffer options, participation rates for the 1% buffer options are 20-25% higher on 1-year strategies and 5-10% higher on 6-year strategies, with all of them being at least 100%. The only other carrier offering a buffer that low is Principal Financial, who goes full-send with a 0% buffer on 6-year S&P 500 and Russell 2000 accounts. Principal’s current par rate on their unbuffered S&P option is 115%. Securian’s par rate on the corresponding 1% buffer option is 116%. Coincidence? I think not. In any case, the opportunity to capture more than 100% of gains in the S&P 500 with no limit on the upside is a powerful story that could draw business not only from other RILAs, but from other investments outside the annuity universe as well.

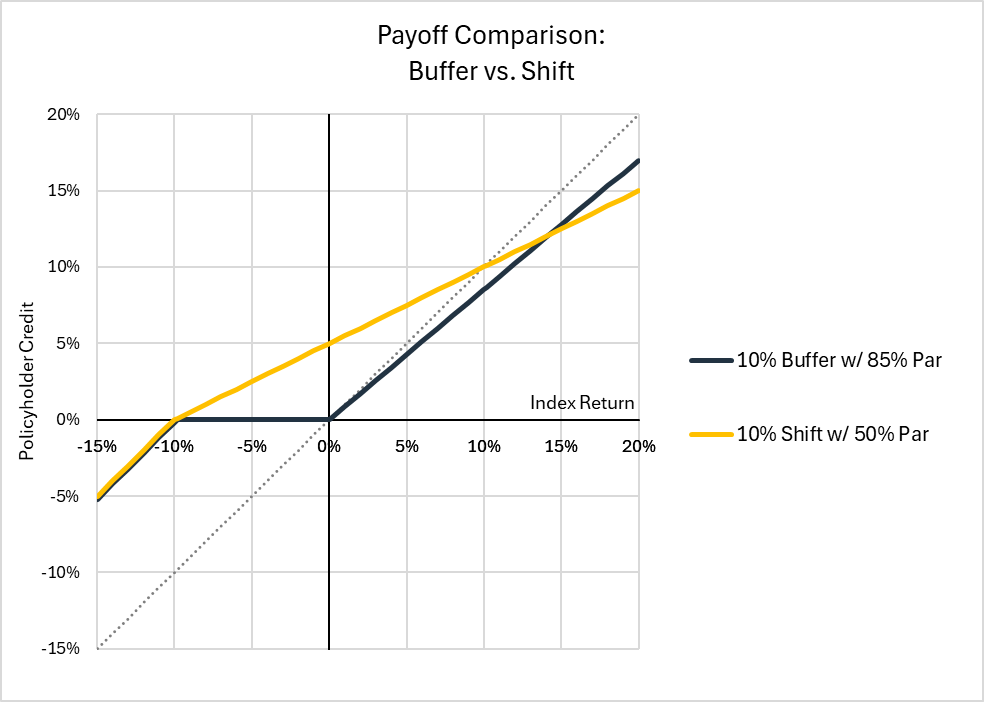

Securian’s contribution to the growing wave of Dual Direction-esque options in the RILA space – which we analyzed extensively in this whitepaper – is the so-called “Shift” strategy, which effectively gives the policyholder a 10% head start on their index returns. The calculation is pretty simple: take the raw index return, add 10%, and apply a participation rate if that result is positive. This mechanism can turn some negative return scenarios into positive credits – for example, an index return of -4% would first be increased by 10%, to +6%. Since the result is positive, the par rate would be applied – currently 50% for a 1-year S&P 500 option – and the resulting index credit would be a positive 3%. A visual comparison to Securian’s corresponding 10% buffer with par option is shown below.

Last but not least, AccumuLink Advance offers an especially unique Accelerated Death Benefit as an optional rider. The rider features a guaranteed 6% compound daily roll-up, along with the ability to accelerate access to the death benefit in the event of Chronic or Terminal Illness. The introduction of this rider marks the first time we’ve seen a roll-up death benefit in the RILA space – let alone one with an acceleration feature. Securian offers versions of this rider on both their FIA and VA chassis, but we’re not aware of another company carrying something similar.

Securian is a conservative mutual company that has never been a huge player in the individual annuity market, posting only about $800M of total annuity sales in 2024. Historically, their focus has been on maintaining their financial strength – which, while enabling them to earn an A+ rating from AM Best for more than 50 years, seems to have hindered their ability to offer the kind of crediting rates that gain market share in this highly competitive environment. But this week’s launch hints that they may be ready to say “no more Mr. Minnesota-nice guy”. The unique features of AccumuLink Advance just might be enough to carve out some room in an increasingly crowded space, and a RILA just might be what it takes to propel Securian toward a broader industry presence. -Drew Schmalz

A Double Digit Rate Hits the MYGA Market

Believe it or not, prospective annuity buyers can now elect to purchase a MYGA from a carrier offering a 10% guaranteed rate in year one. The eye-catching double-digit rate is available on the newly launched 6-year version of Mountain Life’s Secure Summit MYGA. The 10% rate consists of a 5% base rate guaranteed for the entire 6-year term and a 5% rate enhancement in Year 1. Together, the rate pattern amounts to an annual compound equivalent of 5.82% over the 6-year term, which trails only Atlantic Coast Life’s Safe Haven 6 (currently at 5.87%) in the duration, according to AnnuityRateWatch. With only around 20 carriers offering MYGAs in the 6-year duration, this could also be a targeted play at the 5-year and 7-year durations—each home to over a hundred MYGAs.

Mountain Life, rated B+ by AM Best, entered the MYGA market in October of 2024 with the launch of its Secure Summit series. Since then, MYGA product development has continued at Mountain Life. Alpine Horizon launched earlier this summer as the second MYGA in Mountain Life’s suite. Originally available in 3-year and 5-year versions, Alpine Horizon offers a higher top-line rate than Secure Summit but does not provide industry-standard waivers for nursing home confinement or diagnosis of a terminal illness. Last week, Mountain Life added new durations to both MYGAs in their lineup, including the 6-year version of Secure Summit. These additions indicate a desire to focus more heavily on “off-the-run” MYGA durations—those that fall outside of the typical 3-year, 5-year, and 7-year offerings.

In addition to the 11 southern states originally approved Secure Summit back in 2024, Mountain Life has secured approvals from another handful: Maryland, Montana, Nebraska, Ohio, and Oklahoma. Sixteen states remains a small footprint, and Mountain Life’s 2025 sales—on pace for less than $100 million for the year—reflect the constraints facing a B+ rated carrier. While a higher top-line rate offered by the Alpine Horizon design should help drive interest and the added durations may bring Mountain Life MYGAs into new annuity-buying conversations, we expect continued growing pains as the carrier looks to establish itself. Ratings that do not begin with an “A” are difficult to overcome in the annuity market. We’ll see if the allure of a 10% first-year rate is enough to change that reality. -Jon Blomquist

Filing Updates

Inside Equitable’s 72-Form RILA Filing

Based on a massive filing package that was approved by the Interstate Compact last week, Equitable Financial appears to be gearing up for enhancements to their market-leading Structured Capital Strategies (SCS) suite of RILAs. Their current suite, which includes the accumulation-focused SCS Plus 21, the income-focused SCS Income, and the more variable-leaning Investment Edge 21, combined for $7.3B of sales in the first half of 2025 to earn Equitable the top spot on the RILA charts.

The filing includes a mind-blowing total of 72 policy forms – made up of 8 base contracts, 16 sets of data pages, 24 riders, 22 endorsements, and 2 applications. Granted, there are separate sets of forms for each of their two subsidiary carriers, Equitable Financial Life Insurance Company and Equitable Financial Life Insurance of America – the former being used for their New York business and the latter being used everywhere else. But 36 forms per company is still huge. So why so many?

For one, Equitable intends to use combinations of these forms to market not one, but two new products – SCS Plus 25 and SCS Premier. SCS Plus 25 will likely replace SCS Plus 21 as their prevailing accumulation RILA, while SCS Premier appears to be an entirely new product focused on a lesser-emphasized feature in the current RILA landscape – death benefits. More on that later.

Each of the two products will come in multiple share class editions:

- B-share – includes a 6-year Withdrawal Charge period, available on both Plus and Premier

- C-share – no Withdrawal Charges, available on both Plus and Premier

- Advisory – no Withdrawal Charges, sold through fee-based advisors, available on Plus only

Different versions of the base contract and data pages are filed both to accommodate the share classes and provide flexibility in the fee structure Equitable employs. For example, there are 4 different versions of the base contract that represent different combinations of fee structures – with and without Withdrawal Charges, and with and without Contract Fees.

Of the 12 filed riders per company, 8 of them are crediting strategies that will be used on Equitable’s existing selection of well-known market indices. Most of these are refiled versions of strategies offered on SCS Plus 21, which already has an account lineup akin to the menu at a 24-hour diner. However, two of them appear to be brand new:

- Best Entry – This option will reset the starting index value to its lowest point on each of the first 4 monthiversaries in the segment term, subject to a limit of 80% of the actual initial index value. The frequency and duration of observations and the lower limit are all filing placeholders that are subject to change. At the end of the term, the crediting is calculated the same way as a standard buffer/cap strategy, just with a different starting index value as the basis for the performance. Best-entry options, which help reduce market timing risk, have popped up a few times in the industry recently – perhaps most notably in American National’s Smart Start Accumulator FIA.

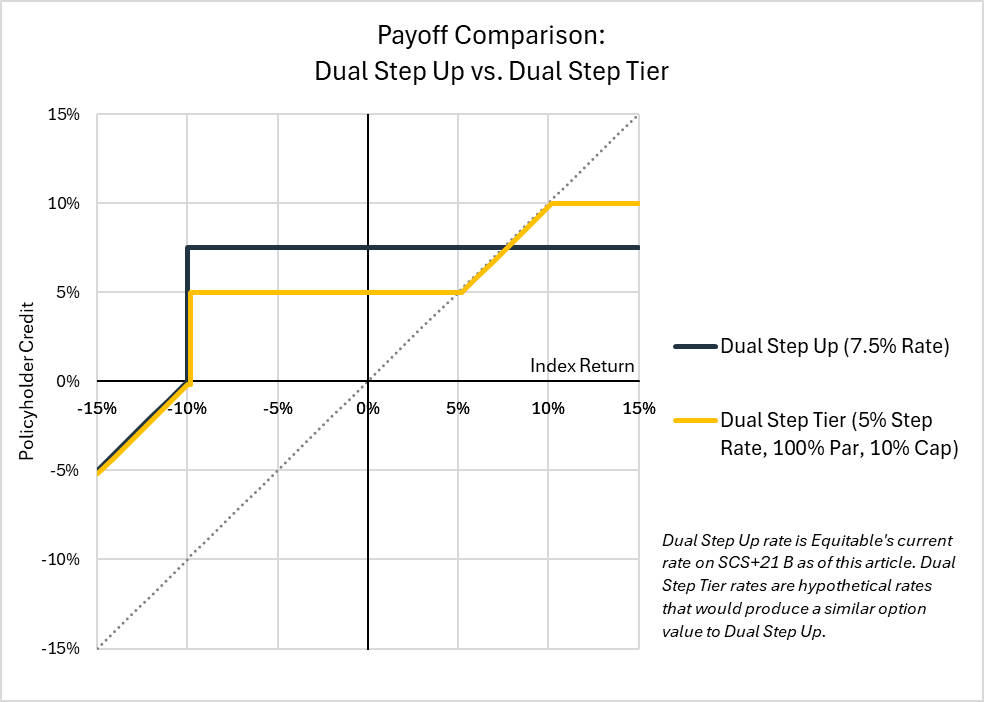

- Dual Step Tier – This is Equitable’s latest innovation in the realm of what we might start affectionately calling “duallies”. Dual Step Tier is similar to Dual Step Up, which is available on SCS Plus 21, except that it offers the opportunity to participate in market gains that exceed the step rate. As long as index returns don’t breach the buffer, you earn a minimum of the step rate (say, 5%), and if returns are greater than that step rate, you earn the index return (subject to a par rate and a cap). Check out the comparison to Dual Step Up below.

The remainder of the riders are death benefits, which are the primary feature that differentiates SCS Premier from SCS Plus 25. The filing includes 4 distinct optional death benefits that are available if the applicant wants more coverage than comes standard:

- Return of Premium (ROP) Death Benefit (SCS Plus 25) – like SCS Plus 21, the standard death benefit is the account value, but the policyholder can elect to purchase the ROP rider for an additional charge. The rider provides a guarantee that the death benefit will be no less than the premium.

- ROP Death Benefit (SCS Premier) – this rider provides the same benefit as the SCS Plus 25 version, but on SCS Premier it will be available at no additional charge.

- Highest Anniversary Value (HAV) Death Benefit (SCS Premier) – this is really where Premier breaks from Plus. Available for a 0.20% charge, the HAV feature locks in the highest account value on any contract anniversary, providing additional protection from the risk of market downturns eroding previously built-up gains in the beneficiary’s inheritance. Until now, Allianz had the only HAV death benefit we’d seen in the RILA market. With this filing, Equitable is getting ready to give them a run for their money.

- Greater of Roll-Up or HAV Death Benefit (SCS Premier) – Why stop at HAV? For policyholders who really want to maximize the amount they pass on to their beneficiaries, SCS Premier will offer a “greater of” rider for a 0.75% annual charge. This tracks both a highest anniversary value and a roll-up value, which accumulates as a fixed 5% simple daily roll-up rate, and sets the death benefit equal to the greater of the two. Thanks to Securian’s recent launch, Equitable won’t be the first to offer a roll-up death benefit on a RILA, but they will be the first we’ve seen to combine it with the HAV component.

Equitable has a reputation to uphold in the ever-evolving RILA market, and with this round of developments they’re working hard to do just that. First, they created the RILA itself – what began as a niche hybrid product has now grown into one of the primary annuity categories, in which almost every major carrier is clamoring for market share. Then, they introduced us to the now-ubiquitous Dual Direction crediting strategy. The development of a standalone product focused on a death protection is their latest “first”. While this one seems less likely to catch fire in the way that other innovations have, it’s clear that Equitable has no intention of giving up its status as the trend-setter of the RILA space – nor its throne atop the sales charts. -Drew Schmalz

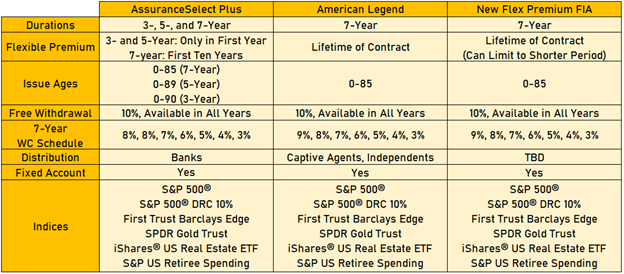

MassMutual Ascend’s Latest Approval? A New Flexible Premium FIA

Last week, MassMutual Ascend—formerly known as Great American—received approval from the Compact for a new FIA product chassis. The flexible premium contract was reviewed and approved for use with several previously approved waivers, riders, and endorsements. The approval of this 7-year flexible premium FIA is curious, as MassMutual Ascend already offers two 7-year flexible premium FIAs: AssuranceSelect Plus and American Legend. Both existing FIAs appear to have had strong starts to the year for the carrier, amassing over $150 million and $300 million in Q1 sales, respectively, according to Beacon Research.

AssuranceSelect Plus is sold exclusively through the bank channel, while American Legend is sold by captive agents and independents. So where is the new FIA headed? Provisions in the contract appear similar to what currently exists with AssuranceSelect Plus and nearly identical to what American Legend offers:

Could this simply be a move to get American Legend onto Compact paper? It’s possible. For a product that generates as much in sales as American Legend, it is surprising that it is continues to be sold on state-by-state forms. Most of today’s FIAs are sold on Compact paper, which makes sense given that the Compact has been reviewing indexed-linked annuities since 2008 and now includes 47 member jurisdictions. As we have seen with existing RILA products being filed with the Compact over the past year, companies value the simplicity of maintaining fewer forms (and thus, fewer state variations) by taking advantage of the Compact’s broad jurisdictional scope. It’s also possible that this new FIA will be deployed alongside the existing products as a distribution-specific variant. Regardless of the strategy, expect MassMutual Ascend to continue pushing toward another multi-billion-dollar sales year in the FIA market. -Jon Blomquist

Weekly Index Spotlight

Guggenheim RBP® Blended Index

Launched – 3/20/2013

Availability – Security Benefit Total Value (no longer available)

Constituents – Guggenheim RBP® Large-Cap Defensive 100 Index, 2-year U.S. Treasury Note Futures

Specs – 6.25% Volatility Target, Excess Return

Decrements – None

In the world of engineered indices, there’s a peculiar paradox: the indices that sound the most boring often end up being the most interesting when you dig into their actual performance. Case in point — the Guggenheim RBP® Blended Index, which has been quietly chugging along since March 2013 with what might be the most compelling track record for FIA applications that nobody talks about.

The core concept is straightforward enough. The index splits its allocation between defensive U.S. large-cap stocks (selected using Guggenheim’s proprietary RBP® methodology) and 2-year Treasury Note Futures. The methodology is a stock-selecting strategy that picks stocks based on their calculated probability that a company will perform well enough to support its current stock price in the future.

As with most balanced, volatility controlled indices, when stock market volatility is low, the index tilts toward equities. When volatility spikes, it shifts toward bonds. The whole thing targets 6.25% volatility and has historically averaged about a 50/50 stock/bond split. It’s the investment equivalent of putting on a sweater when it gets cold — practical, systematic, and utterly unsexy.

But here’s where it gets interesting. While other engineered indices from the same era have been busy chasing the latest investment themes or layering on complexity to justify their existence, Guggenheim RBP has been delivering something that’s become increasingly rare in the indexed annuity world: consistent positive returns. Over the past decade-plus of live performance, the index has posted positive returns in eight out of ten calendar years. The two negative years? 2018 (-0.55%), and 2022, when it dropped 9.2% — a respectable showing considering the S&P 500 was down over 18% that year.

That 80% positive return rate over the last ten years isn’t an accident. It’s the direct result of the index’s defensive positioning. The RBP® stock selection methodology screens for companies with low beta characteristics and strong business fundamentals. These aren’t the high-flying growth stocks that dominate headlines; they’re the boring, steady companies that tend to hold up better when markets get choppy. Paired with short-duration Treasury exposure, the index is essentially built to avoid the dramatic drawdowns that plague pure equity strategies.

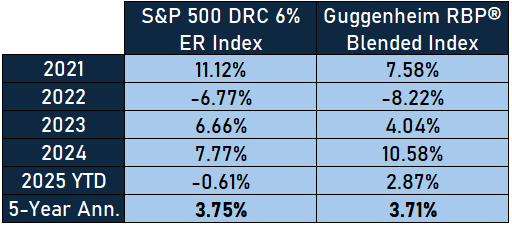

So how does it stack up against the relevant benchmarks? The closest comparison is the S&P 500 Daily Risk Control 6% Excess Return index, given the similar volatility target and structure. Over the past five years, Guggenheim RBP has delivered a 3.71% annualized return – extremely close to the benchmark’s 3.75%.

The allocation mechanism is refreshingly transparent. Every day, the index calculates the 20-day realized volatility of its stock component and adjusts the allocation accordingly. More volatility means more bonds, less volatility means more equities. There’s no black box algorithm or mysterious “regime detection” — just a straightforward mathematical formula that responds to market conditions.

That’s not to say the index is without complexity. The RBP® stock selection methodology adds a layer of sophistication beyond basic volatility control. The system attempts to identify companies most likely to meet “Required Business Performance” targets using probability calculations. It’s more nuanced than simply buying the S&P 500, but it’s also more systematic than active stock picking. The question is whether this complexity adds value or just creates noise.

Based on over a decade of live performance, it appears to add value. The index has delivered its returns primarily through systematic beta exposure — the natural result of dynamically allocating between stocks and bonds based on volatility. But there’s also a modest alpha component from the stock selection process that seems to have held up over time. Unlike many engineered indices where the performance comes from backtested optimization that falls apart in live trading, Guggenheim RBP has validated its approach through multiple economic cycles.

The timing of the index’s launch was fortuitous. March 2013 marked the beginning of one of the longest bull markets in history, but also a period of rising interest rates and increasing market volatility in later years. The index navigated the 2015-2016 market correction, the 2018 sell-off, the 2020 pandemic crash, and the 2022 bear market while maintaining its defensive characteristics. That’s not backtested performance — that’s real-world validation across diverse economic environments.

Of course, defensive positioning comes with trade-offs. The allocation to the underlying index is capped at 100%. Put another way, no leverage can be used to obtain more equity exposure if volatility is extremely low. The index’s 6.25% volatility target inherently limits upside participation during strong equity rallies. While the S&P 500 was posting double-digit gains in recent years, Guggenheim RBP was delivering mid-to-high single-digit returns. For investors chasing maximum returns, that’s frustrating. For FIA policyholders focused on consistent crediting, it’s exactly what they need.

The index also carries the typical challenges of Excess Return structures. By deducting the risk-free rate from performance, it creates scenarios where the index can show negative returns even when underlying assets perform well, particularly during periods of inverted yield curves. It’s a trade-off that makes the options cheaper and allows for higher participation rates, but it also makes the performance harder to explain when things go sideways.

Perhaps the most intriguing aspect of Guggenheim RBP is how little attention it receives relative to its track record. In an industry obsessed with the latest innovations and marketing gimmicks, a boring balanced index that simply does what it says it will do doesn’t generate much buzz.

As interest rates have risen and fallen, as growth stocks have soared and crashed, as market volatility has spiked and subsided, Guggenheim RBP has maintained its steady approach. It’s not going to be the best-performing index in any given year, but it’s also unlikely to be the worst. What it has shown is that it can consistently deliver positive returns. For FIA applications, that predictability is worth its weight in gold.

Guggenheim RBP used to be offered on Security Benefit’s Total Value annuity, but that product has been put out to pasture. As an index with such a strong live performance, why is it nonexistent in the FIA market today? It would be wise, from our perspective, for someone to snatch this index up and put it back where it belongs: within FIAs. -The Index Spotlight Team

Benchmarks

Fair-Market S&P 500 Caps and Participation Rates

| Date | Option Budget | S&P 500 Cap Rate | S&P Par Rate |

| 8/29/2025 | 5.01% | 9.67% | 63.87% |

| 8/22/2025 | 5.02% | 9.47% | 62.04% |

| 8/15/2025 | 4.95% | 9.57% | 63.57% |

| 8/8/2025 | 4.97% | 9.55% | 62.70% |

| 8/1/2025 | 5.07% | 9.64% | 62.92% |

| 7/25/2025 | 5.11% | 9.91% | 64.23% |

| 7/18/2025 | 5.20% | 9.96% | 63.79% |

| 7/11/2025 | 5.13% | 10.01% | 64.23% |

YTD Index Returns (as of 8/28):

- S&P 500: 10.79%

- Nasdaq: 13.00%

- Dow Jones: 7.65%

Treasury Yields (week over week change, as of 8/28)

- 1-year: 3.85% (-10 bps)

- 2-year: 3.62% (-17 bps)

- 3-year: 3.60% (-15 bps)

- 5-year: 3.69% (-17 bps)

- 10-year: 4.22% (-11 bps)

- 20-year: 4.83% (-6 bps)

- 30-year: 4.88% (-4 bps)

[/mepr-show]